Obesity is a critical public health challenge in the UK, with two-thirds of adults now living with excess weight, and levels of childhood obesity in the UK among the highest in Europe. In January 2026, the government implemented new statutory restrictions on advertising for less healthy food and drink, covering products high in fat, salt and sugar (HFSS) within certain categories, banning paid adverts on TV before 9pm and online at any time.

This report explores the changing face of food and drink advertising, and assesses how much of it falls within the scope of the new regulations on less healthy food and drink advertising.

It identifies several exemptions to the policy and sets out the effect they are likely to have on how the policy works. The report also highlights the role of industry influence on the ambition and timeline of the policy, which has contributed to its weakened potential health impact.

What’s in the report

- We look at how food and drink advertising spend has changed over the last two decades. While total spend has been relatively constant during this time, increasing by around 7% in real terms between 2004 and 2024, this disguises a likely rise in our exposure to food and drink advertising, driven by a shift from broadcast TV to cheaper, harder-to-avoid digital and outdoor channels.

- We explore how the current legislation contains several major gaps. These include exemptions for adverts for food and drink brands (as opposed to specific products) and ranges of products; the exclusion of outdoor advertising, a fast-growing channel; the narrow set of 13 food and drink categories covered, and the exclusion of owned media and direct digital marketing, such as brands’ own websites, apps and direct messaging.

- In a deep dive on direct digital marketing, we demonstrate that younger and more deprived groups face higher exposure and more aggressive tactics: 22% of people receive three or more food and drink marketing messages each day, and 64% of messages promote an unhealthy brand or product. People in the most deprived areas receive nearly 50% more marketing from less healthy food and drink brands than those in the least deprived areas.

Findings/recommendations

- We estimate that the current restrictions will affect 8% of food and drink advertising spend. This could fall to as little as 1% once likely shifts of spend into unregulated channels and advertising types are accounted for.

- However, if the government were to close the loopholes which currently exist by including outdoor advertising, unhealthy brands and ranges, and less healthy products outside of the 13 food and drink categories included in the current policy, we estimate restrictions would affect up to 33% of total food and drink advertising spend.

- Closing these loopholes would strengthen the impact of existing restrictions by limiting companies’ ability to shift spending into exempt channels or formats, and encouraging greater promotion of healthier food and drink.

- Another public health measure, the healthy food standard policy, was announced by the UK government last year. It has the potential to deliver a step-change in obesity reduction in the UK, but to achieve this, it is crucial that this policy is implemented as quickly and impactfully as possible. To avoid the delay and dilution seen with the advertising regulations, we recommend the government sets an implementation timeline in legislation and holds to it, and establishes critical definitions and scope in legislation introducing the requirement.

Advertising regulations

Image Description

Three pie charts presenting advertising regulations in the UK.

Chart 1: Current Regulatory Impact

Pie chart titled "Currently, 8% of total food and drink advertising spend are impacted by January 2026 regulations." The chart shows two segments: 92% of advertising spend is "Unaffected" (blue) and 8% is "Impacted" (yellow). Source: Nielsen Ad Intel Report.

Chart 2: Impact After Redirection

Pie chart titled "However, when considering the proportion likely to be redirected to brand or outdoor advertising, only 1% of food and drink advertising will be affected." The chart shows three segments: 92% is "Unaffected" (blue), 7% is "Likely to be redirected" (grey), and 1% remains "Impacted" (yellow). Source: Nielsen Ad Intel Report.

Chart 3: Estimated Impact of Revised Regulation

Pie chart titled "By closing the loopholes in the regulation, we estimate that a third of food and drink advertisements could be covered." The chart shows two segments: 67% of advertisements are "Unaffected" (blue) and 33% fall under "Revised regulation impact" (green). Source: Nielsen Ad Intel Report.

- Executive summary

- Part I – Why food and drink advertising matters

- Part II - The size and scale of food and drink advertising and the limitations of the current advertising restrictions

- Data and methods

- Key point 1: Total food and drink advertising spend has remained relatively stable over the last 20 years, but exposure has likely increased.

- Key point 2: The exclusion of outdoor advertising leaves a significant loophole for displacement into a channel which is already a major source of unhealthy food advertising

- Key point 3: Large proportions of food and drink advertising spend are focused on driving consumption of HFSS products, yet the government's current definition of less healthy food and drink excludes a significant proportion of products that are HFSS.

- Key point 4: The brand exemption leaves 36% of food and drink advertising untouched by current regulations; the additional impact of range advertising is unknown and could further widen this gap.

- Key point 5: Owned media is rapidly evolving and growing, but the scale and impact of this is unknown

- Part III - Implications for current and future policy

- Key point 1: We estimate that current restrictions cover just 8% of food and drink advertising spend, and once displacement to unrestricted channels and brand-focused advertising is accounted for, they are likely to affect only around 1% of food and drink advertising spend.

- Key point 2: We estimate that closing the loopholes which currently exist could lead to 33% of food and drink advertising spend being in scope of regulations.

- Key point 3: The government should take and implement lessons from the policy development of the current advertising restrictions.

- Key point 4: The new government Nutrient Profiling Model (NPM) will increase the impact of both current advertising regulations and the healthy food standard. However, given the potential oversized impact of the healthy food standard, applying the new NPM to policy must not delay the healthy food standard's implementation.

- How could the government make the restrictions more watertight?

- Appendix 1: Method to investigate the proportion of ad spend covered by recent advertising legislation

- Endnotes

Executive summary

Obesity is a critical public health challenge in the UK, with two-thirds of adults now living with excess weight. In response, in January 2026, the government implemented new statutory restrictions on advertising for less healthy food and drink, covering products high in fat, salt and sugar (HFSS) within certain categories, banning paid adverts on TV before 9pm and online at any time.

The implementation of this policy has been significantly delayed and the restrictions are significantly less impactful than they could be because of multiple scope and design limitations, including exemptions for brand and range advertising, the exclusion of outdoor media, narrow product definitions, and the focus on paid-for advertising only. Plans for this policy were first announced eight years ago, and since then, there have been eight consultations and four delays to implementation. Over this period, the policy has been narrowed through changes made following consultation, as well as decisions taken outside formal consultation.

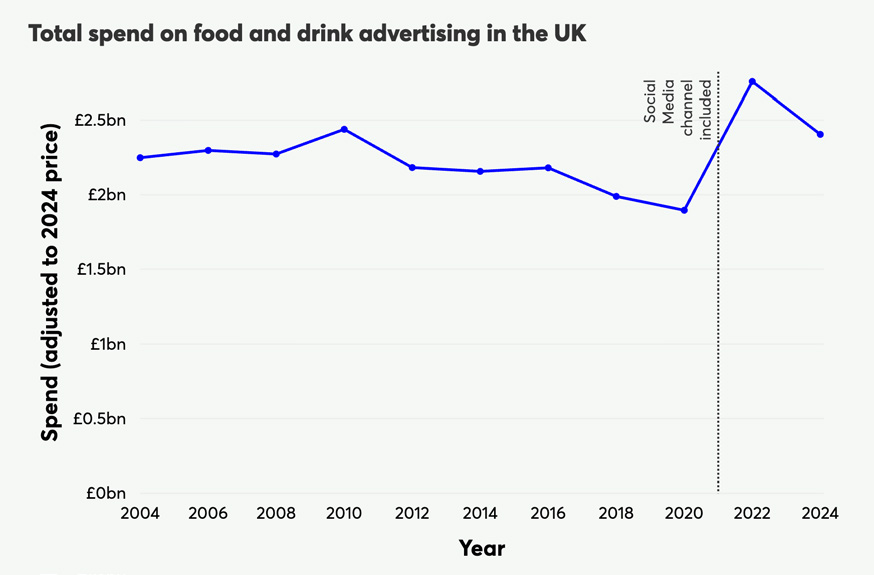

Total food and drink advertising spend has been relatively constant over the past two decades, increasing by around 7% in real terms between 2004 and 2024 (from £2.25 billion adjusted to 2024 prices to £2.41 billion). However, stable food advertising budgets disguise a likely rise in exposure, driven by a shift from broadcast TV to cheaper, harder-to-avoid digital and outdoor channels.

The omission of outdoor advertising in current restrictions is significant given the scale and growth of spend on this channel and the risk of displacement of spend into it following implementation of restrictions: whilst TV food and drink advertising spending has fallen by 40% in real terms since 2004 (from £1.4 billion to £847 million), outdoor advertising has expanded substantially, rising from £197 million in 2004 (in 2024 prices) to £651 million in 2024, and by 59% between 2018 and 2024 (ie, since the recent restrictions were first announced).

41% of consumer spend in large supermarkets is on HFSS products. However, because the regulations apply only to 13 food and drink categories defined by the UK government as being of most concern to childhood obesity, around 60% of advertising spend on HFSS products falls outside these restrictions[^1].

Current restrictions leave brands and ranges exempt: 36% of food and drink advertising spend (£824 million) is already brand-focused. It is unclear to what extent advertising that could be characterised as product "ranges" is captured in this figure, meaning the true share falling outside the scope may be higher. The evidence base is limited but suggests it is likely that brand-only advertising does increase consumption, though it remains unclear how this impact compares to product-specific advertising.

Current regulations completely exempt owned media channels (those which are controlled directly by brands, such as their websites, apps and direct messaging), which are the most rapidly evolving forms of advertising. However, their scale and impact are poorly understood. In a deep dive on direct digital marketing, we demonstrate that younger and more deprived groups face higher exposure and more aggressive tactics: 22% of people receive three or more food and drink marketing messages each day, and 64% of messages promote an unhealthy brand or product. People in the most deprived areas receive nearly 50% more marketing from less healthy food and drink brands than those in the least deprived areas.

We estimate that the current restrictions will affect 8% of food and drink advertising spend. When factoring in expected displacement to non-restricted media channels and from product to brand advertising, we estimate the regulations will, in fact, only affect around 1% of total food and drink advertising spend, which is roughly equivalent to the annual advertising budget of a single company like Domino's Pizza. It remains unclear whether this spend will be redirected towards healthier products, shifted into other forms of marketing, or absorbed elsewhere.

However, if the government were to close the loopholes which currently exist by including outdoor advertising, unhealthy brands and ranges, and less healthy products outside of the 13 food and drink categories included in the current policy, we estimate restrictions would affect up to 33% of total food and drink advertising spend. Closing these loopholes would strengthen the impact of existing restrictions by limiting companies' ability to shift spending into exempt channels or formats, and encouraging greater promotion of healthier food and drink.

Earlier this year, the government published a long-awaited update to the Nutrient Profiling Model, which estimates suggest could increase the impact of current policies by up to 30%. However, with so much at stake, applying the new NPM to policy must not delay implementation of the healthy food standard, which, by requiring large food businesses to meet mandatory targets to improve the healthiness of their sales, could have an oversized impact, helping around 3 million people achieve a healthier weight.

Part I – Why food and drink advertising matters

The obesity challenge & why advertising is relevant

Nearly two-thirds of adults and one-third of children in the UK are living with obesity or excess weight, costing the UK economy and wider society an estimated £126 billion annually. Obesity is a solvable issue. To halve obesity prevalence requires those living with excess weight to reduce their daily calorie intake by 8.5%, or 216 calories, roughly equivalent to a single slice of medium pepperoni pizza. This is a modest shift, but one that is difficult to achieve in a food environment designed to push us towards less healthy options. Advertising is one part of a broader set of food marketing practices – such as product design, pricing, promotions and direct engagement – which together play a key role in shaping what we buy and eat, and ultimately our risk of obesity.

In January 2026, the government implemented new restrictions on the advertising of food and drinks that are high in fat, salt, and sugar (HFSS) within certain high-risk food and drink categories, banning paid adverts on TV before 9pm and online at any time across the UK. Designed to tackle obesity, these measures mark a significant intervention in the UK's food environment. However, the media landscape has evolved substantially since these policies were first conceived eight years ago, and moving from conception to implementation has been a complex process involving significant modifications in scope. Despite the scale of these changes, there remains limited up-to-date evidence on whether the new restrictions reflect how people now encounter food and drink advertising.

This report explores the extent to which the new less healthy food and drink advertising restrictions are likely to deliver a reduction in exposure to unhealthy food and drink advertising. Combining media research company Nielsen's Ad Intel data on advertising spend and new data on exposure to direct digital marketing with expert opinion on emerging industry trends, we compare the current lie of the land with regard to advertising in 2024, how the sector has changed over the last 20 years and identify opportunities to strengthen current restrictions for more effective advertising policy.

We cover both traditional advertising – such as TV, billboards and webpage sidebars - and direct digital marketing delivered via email, app notifications or SMS, reflecting the growing integration of these channels and their shared goal of influencing food and drink purchases.

The rest of Part I explains the role that advertising shapes what we eat, and lays out the details of the latest restrictions on advertising for unhealthy food and drinks.

How food and drink advertising shapes what we eat

Advertising contributes to rising obesity when it encourages us to consume more energy in the form of calories than we use. Some argue that advertising predominantly drives brand switching – substituting one product for a similar product from another brand – and therefore won't affect overall calorie intake. However, growing evidence shows that advertising can increase calorie consumption. The evidence is strongest for children, where experimental studies show higher calorie intake after exposure to food and drink advertisements, but emerging studies suggest adults are similarly influenced, with advertising increasing desire for whole categories of food and drinks, like fast food, soft drinks or confectionery, not just specific brands.

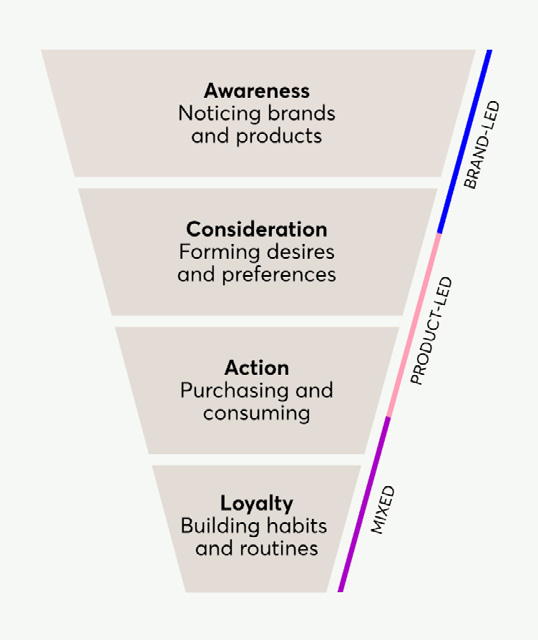

Food and drink marketers use a variety of persuasive techniques – including time-limited promotions, seasonal nudges, and targeted digital advertising – to raise awareness, create desire, encourage initial purchases, and build long-term loyalty that drives repeated consumption; this process is often illustrated as a funnel (figure 1).

Figure 1: The marketing funnel and the relative roles of brand and product-focused advertising

Derived from classic advertising models such as AIDA, the marketing funnel is a means of conceptualising how marketing activity moves customers from awareness to action. This adapted version is used to indicate where brand-led and product-led advertising typically operate along this journey.

This report differentiates between brand advertising, which generally builds familiarity, and product advertising, which aims to trigger more immediate purchases. While evidence suggests that product advertising consistently drives calorie consumption, the picture for brand advertising is less clear. Evidence shows that exposure to brand-only food and drink advertising can influence children and young people's preferences and intentions to consume, suggesting a possible role in shaping consumption. However, direct causal evidence on the impact of brand-only advertising on actual intake is scarce. A recent review found that no existing studies looked at the impact of advertising on consumption specifically, and many of those that focused on the impact of brand marketing had important methodological limitations. The small amount of reliable research shows mixed findings: some studies suggest brand marketing is less impactful than product marketing on immediate purchase intentions, while other emerging evidence indicates they may be just as effective at driving consumption. Overall, while it is likely that brand-only advertising has some influence on consumption, it remains unclear how this impact compares to product-specific advertising.

Not all food and drink advertising is harmful; it could potentially even be a powerful tool for promoting healthier eating. However, previous evidence suggests that nearly half of TV food and drink advertising is driving consumption towards less healthy products. This exposure is unequal: lower socioeconomic groups encounter a far higher volume of overall advertising, particularly on traditional media (eg, TV, outdoor), resulting in twice as much exposure to unhealthy food messaging as more affluent groups. This disparity is amplified both by online advertising for unhealthy foods being directed towards people on lower incomes based on information collected about users, including past behaviour and engagement, and greater reliance on public transport in deprived areas, which increases exposure to the proliferation of unhealthy foods advertising across transit networks.

The current policy landscape and its loopholes

The new regulations, which came into force in January 2026, apply across the UK and restrict advertising of products high in fat, salt, or sugar (HFSS) that fall within certain food and drink categories – according to the UK government's Nutrient Profiling Model threshold – for large businesses[^2] across the following channels (noting an exemption for small and medium enterprises):

- Broadcast TV: Advertising is prohibited before the 9pm[^3] watershed[^4].

- Paid-for online advertising: Restrictions apply to any web space where a brand pays to be featured on a third-party platform at any time of the day. This includes website banners, paid search engine results, ads interrupting video content, sponsored posts on social media, but excludes a brand's own direct channels (like their website, app, non-sponsored social media content, or customer emails and SMS).

These regulations apply only to HFSS products in 13 predefined food and drink categories, including sweet biscuits, confectionery, desserts, crisps, ready meals and breakfast cereals, identified by the UK government to be of most concern for childhood obesity, rather than all HFSS products.

These new statutory restrictions build on longstanding self-regulatory advertising codes of practice, which had already set a limit on HFSS advertising across TV, online and outdoor media where children make up a significant share of the audience.

These advertising restrictions were established in the Health and Care Act 2022, which amends the Communications Act 2003. To implement this, the government introduced several pieces of legislation. The Advertising (Less Healthy Food Definitions and Exemptions) Regulations 2024 set the legal definition of which products count as 'less healthy', while the Advertising (Less Healthy Food and Drink) (Brand Advertising Exemption) Regulations 2025 clarified when companies may continue to run brand-only advertising that does not feature HFSS products. Additional implementation and enforcement regulations enable Ofcom and the ASA to monitor and police the new restrictions.

Since plans for this policy were first announced eight years ago, there have been eight consultations[^5], four delays to implementation and the potential impact of the policy has been significantly reduced through choices made as a result of consultation.

On the next page, we present the entire journey regulations have taken from first proposal to coming in to force.

Policy Implementation Timeline

2018

UK government first proposes introducing regulations to ban HFSS advertising pre-watershed (9pm) on TV and online as part of their Childhood Obesity Plan.

2019

UK government's DHSC and DCMS jointly consult on whether to extend existing advertising restrictions to a pre-watershed (9pm) ban on HFSS advertising on TV and online.

2020

In July, the government announce its intention to implement a ban on HFSS product advertising on TV before 9pm and online 24/7.

A second government consultation seeks views on a total online ban, the type of advertising and marketing in scope (eg, brand/product, direct emails, unpaid promotions), enforcement and liability.

June 2021

The government publishes its response to the 2019 and 2020 consultations (2 years since the former) and commits to a 9pm TV watershed and 24/7 online ad ban, reporting the regulations expected to come into force by the end of 2022. It indicates that, following industry feedback, unpaid online media (brands' own social media and websites, and direct email marketing) is no longer in scope.

March 2022

Following industry lobbying, regulations were delayed until January 2024 to allow businesses time to prepare. Industry claimed at least one year needed from when guidance is published by the Committee of Advertising Practice, the body tasked with interpreting the law.

April 2022

The first legislative step is achieved via the passing of the Health and Care Act 2022, which gave new powers to the existing Communications Act 2003 to enable the new advertising restrictions via secondary legislation.

December 2022 – March 2023

Announcement of draft legislation in December 2022 gives practical effect to provisions on advertising enabled by the Health and Care Act. Known as The Communications Act 2003 (Restrictions on the Advertising of Less Healthy Food) (Effective Date) (Amendment) Regulations 2022 (SI 2022 No. 1311)

The government consults on the draft legislation, seeking views on products and businesses in scope.

Enforcement delayed to 2025. Response to industry and regulator (Advertising Standards Authority) feedback that delays to Royal Assent of the Health & Care Act meant there was insufficient time for industry to prepare for January 2024 enforcement.

December 2023 – February 2024

Advertising Standards Authority (ASA) launches consultation on draft guidance for how the restrictions will be applied.

September 2024

The government publishes a response to the consultation on the draft legislation and conducts an additional technical consultation on the application of the rules to Internet Protocol TV (eg, Netflix, YouTube).

December 2024

ASA publishes definitive guidance for how advertisers should apply the regulations.

The Advertising (Less Healthy Food Definitions and Exemptions) Regulations 2024 laid before Parliament in December 2024 with a planned enforcement date of 1 October 2025.

January - February 2025

ASA publishes new draft guidance, which adopts a more cautious interpretation of the legislation. It suggests that some brand-only ads without identifiable HFSS products might still fall within the scope of the regulations if they could reasonably be interpreted as being associated with an in-scope product (eg, brands synonymous with HFSS).

ASA opens a further consultation seeking views (industry, third sector and other) on the latest guidance.

May - September 2025

The government responds to industry pressure by placing a 'brand exemption' on a statutory footing via The Advertising (Less Healthy Food and Drink) (Brand Advertising Exemption) Regulations 2025.

Implementation is delayed to January 2026, with voluntary industry rollout requested from October to allow time for further consultation by the government and the ASA. Brand-only ads, including the brand of a range of products, are exempt, provided no identifiable HFSS product is featured.

December 2025

ASA publishes definitive guidance for how advertisers should apply the regulations.

January 2026

Regulations come into force – three years after initially planned and eight years after the concept was announced in policy.

While industry consultation is necessary for advising on how policy is delivered, it is evident that in this instance, the process has allowed industry to dictate the ambition and timeline of critical measures to tackle obesity. This influence did not happen in a vacuum. Between 2010 and 2023, ministers met with food businesses and their trade associations around 40 times more often than with food NGOs and public-interest organisations. In part III, we discuss what can be learnt from the development and implementation of the advertising ban to inform the implementation of the government's recently announced healthy food standard.

The subsequent section presents new research illustrating how the decisions made in implementing the current restrictions have led to a regulatory landscape which will have a significantly lower impact on public health than it might have. This is due to four key factors:

- The brand exemption means that any company brand advertising, as well as "the brand of a range of products" (eg, ranges like McDonald's 'Happy Meals' or Cadbury's 'Dairy Milk') can continue to be advertised on all channels irrespective of the health of the brand or products within the range advertised (see page 23 for examples).

- By focusing on pre-watershed TV and online advertising, the restrictions leave several other important media channels – most notably outdoor (eg, billboards and bus stops) unaffected. This means advertising spend can, if needed, be redirected to unrestricted channels and will continue to drive consumption of unhealthy food and drinks.

- By focusing on only 13 food and drink categories, the restrictions leave out a large number of HFSS products (as defined by the UK government's Nutrient Profiling Model).

- By focusing exclusively on paid-for advertising, ie, owned and direct marketing channels remain unregulated.

Part II - The size and scale of food and drink advertising and the limitations of the current advertising restrictions

Data and methods

Findings on paid-for advertising are based on analysis of 20 years of UK food and drink (including alcohol)[^6] advertising data from Nielsen Ad Intel (see technical report for methodology). For the period between 2020 and 2024, we were able to analyse a more detailed breakdown covering the advertising spend for over 5,200 food and drink companies in the UK, including supermarkets, manufacturers, delivery apps, and large out-of-home chains.

The granularity of available data did not allow us to directly estimate advertising spend that was focused on products that are HFSS according to the government's NPM threshold. As a proxy for the proportion of advertising spend, we used data from Worldpanel by Numerator's GB Take Home panel (over the period 1st January to 31st December 2024) to estimate the proportion of consumer spend and calories purchased both within the 13 in scope categories and outside of these categories that are from HFSS products.

Findings relating to digital and direct messaging are derived from our own data collection, in which we tracked food and drink direct digital marketing using a multi-day diary study with a representative sample of over 1,500 adults. Each participant completed one diary day, together providing seven days of independent observation. This resulted in a dataset of 2,400 marketing emails, push notifications and texts from over 500 brands. This reveals how much food and drink direct digital marketing (DDM) people receive, which brands and products are promoted, and the tactics used to promote them (see technical report for more information).

Expert insights reported were derived from a series of 1-hour-long semi-structured qualitative interviews with eight advertising and food marketing experts covering a breadth of industry roles. The aim was to identify critical shifts in advertising strategies and practices based on first-hand experience. Interview transcripts were analysed using qualitative thematic analysis. See the technical report for further details.

Key point 1: Total food and drink advertising spend has remained relatively stable over the last 20 years, but exposure has likely increased.

Total food and drink advertising spend has been relatively constant over the past two decades, increasing by around 7% in real terms between 2004 and 2024 (from £2.25 billion adjusted to 2024 prices to £2.41 billion; figure 2).

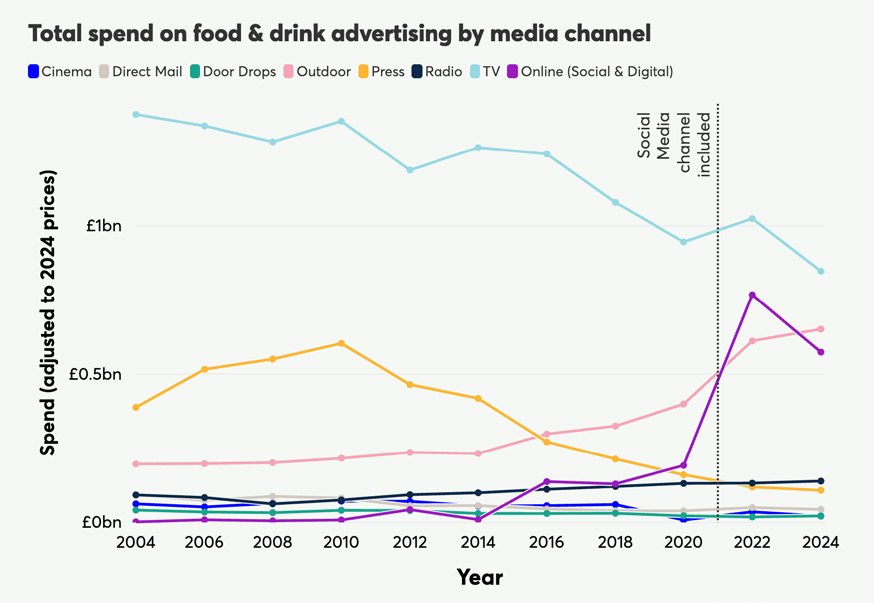

However, there has been a shift in the media channels on which this spend has been focused: although still the largest single channel, TV spending has fallen by 40% in real terms since 2004 (from £1.4 billion to £847 million; figure 2), and by 21% between when the recently implemented less healthy food and drink advertising restrictions were first announced in 2018 and 2024. At the same time, spend has shifted towards both online channels and outdoor spaces: in real terms, online advertising (social and other digital combined) has grown from a tiny £1.7 million in 2004 to £574 million in 2024. Outdoor advertising, which is unaffected by the recent advertising restrictions, has also expanded substantially, rising from £197 million in 2004 (in 2024 prices) to £651 million in 2024. More recently, outdoor advertising spend increased by 59% between 2018 and 2024, and by 33% between 2021 and 2024; the latter is in line with findings from the Food Foundation, which estimated 28% growth in spend over this period (we discuss outdoor advertising in more detail on page 18).[^7]

Figure 2. Total spend on food and drink advertising by media channel 2004-2024.

Online advertising combines Nielsen's estimates for social and digital advertising spend, with social media spend only added in 2021.

While aggregate Nielsen data suggests that real-terms expenditure on food advertising has remained relatively stable, this 'monetary input' does not necessarily reflect consumer exposure to advertising due to fundamental shifts across advertising as a whole during the period.

In the past 20 years, the way we are exposed to advertising has changed dramatically. In 2004, TV and radio advertising spend made up 65% of total food and drink advertising; by 2024, this had decreased to 40%. Meanwhile, outdoor advertising spend is now three times greater in real terms, alongside the emergence of social and digital channels, which make up 27% of total spend. Two decades ago, avoiding unhealthy advertising was largely a matter of turning off your TV or radio. Today, investment in a broader range of channels means we are bombarded by advertising in every aspect of our physical and digital lives. This constant exposure makes it far harder to tune out unhealthy prompts, creating an environment that shapes our choices and drives us to over-consume.

The cost of reaching audiences on traditional broadcast TV has risen disproportionately compared to other channels. The cost-per-thousand views (CPT) increased by around one-third between 2019 and 2022, and a further 28% spike in TV costs in 2024 (not inflation-adjusted) alone due to declining viewership. As a result, advertisers have shifted budgets toward other formats offering lower cost per exposure and higher potential reach (eg, online and outdoor advertising). Whereas TV CPT is reported at £20-25, for OOH and digital media it is considerably lower with ranges reported of £2-20 for outdoor billboard and £3.50-8 for online/social media, depending on format and targeting (we note that exposure to different advertising channels will have different levels of intensity/ impact on our behaviour). Digital channels now account for approximately four out of every five pounds spent on all advertising (not just food). Even outdoor advertising is changing in a way that increases exposure: Outsmart data, from the industry database of available outdoor inventory reports an increase of digital OOH screens from 12K-41K between 2018 and 2025. These screens run multiple ads in a single location (typically 6-10/min), increasing the number of ads the public encounters there.

While the precise volume of advertising exposure among UK consumers is hard to measure, evidence from the UK's advertising regulator suggests there may have been a substantial increase in advertising activity – and consequently exposure – over the past two decades. The number of advertisements investigated by the ASA more than doubled between the mid-2000s and 2018. This reflects what the ASA itself describes as an evolving advertising landscape in which ads are "generated and placed ... in millions of executions every day by tens of thousands of advertisers and content creators." To manage this scale, the ASA radically changed its monitoring approach, adopting automated, AI-powered systems.

Taken together, these trends suggest that despite apparently stagnant advertising budgets, consumers may well be exposed to food advertising more frequently than ever before.

Key point 2: The exclusion of outdoor advertising leaves a significant loophole for displacement into a channel which is already a major source of unhealthy food advertising

The focus of the recent less healthy food and drink advertising restrictions exclusively on pre-watershed TV and online advertising leaves a substantial portion of the spend (51%) unaffected by the recent advertising restrictions. The gap creates a clear opportunity for brands to redirect their budgets. Analysis published by the UK government suggests that around 81% of HFSS spend removed from TV and online will be displaced to other formats; the greatest share (26%) is expected to move to outdoor advertising, followed by print (22%), radio (15%), and cinema (15%).” These estimates were made in 2021, before the full implications of the brand exemption were understood.

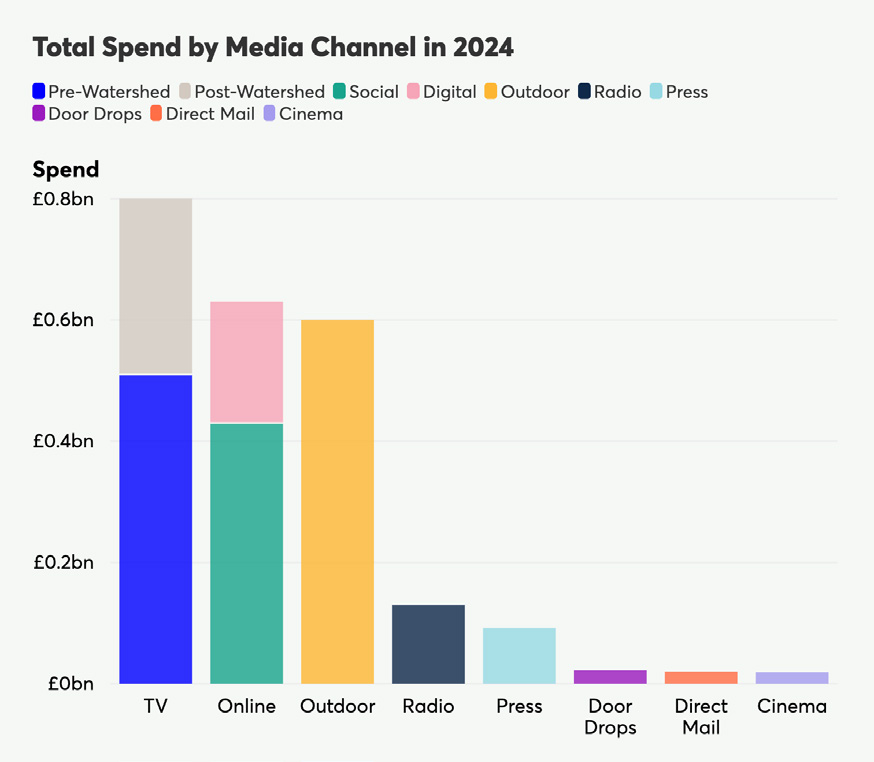

Outdoor advertising (eg, billboards and bus stops), which currently accounts for 27% (£590 million) of food and drink advertising spend (figure 3), is the most notable exclusion from current restrictions, having more than tripled over the last two decades. Industry further claims that 98% of the public sees a billboard at least once a week, highlighting the very high reach of outdoor advertising. Designing restrictions around a declining medium like TV while leaving a growing, high-impact medium like outdoor advertising untouched risks creating a policy geared towards the past, not the future.

Figure 3. Food and drink advertising spend in 2024 by media channel

2.1 Outdoor advertising is a significant source of unhealthy food advertising

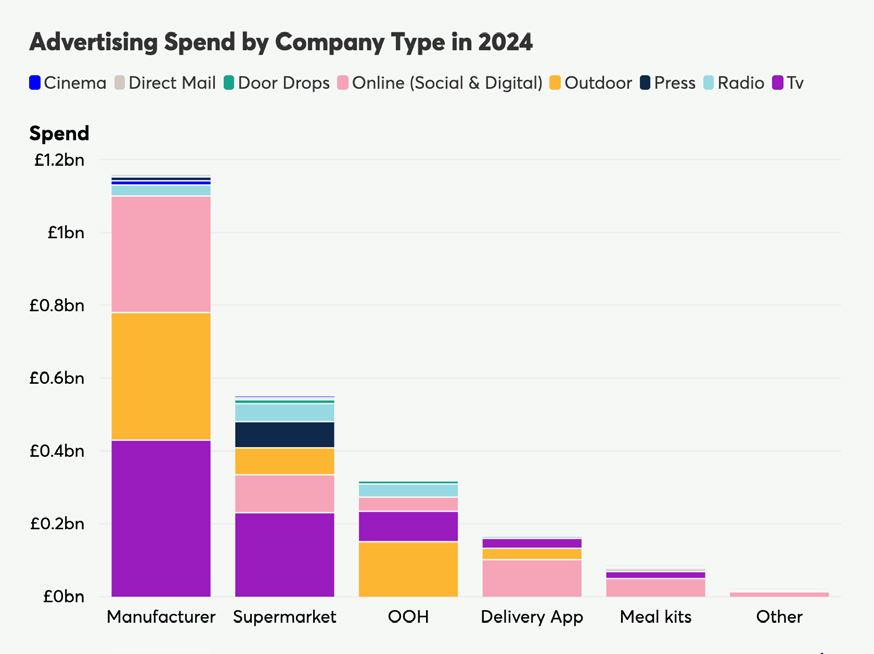

Outdoor media (eg, bus stops, buses and billboards) is particularly important because it is disproportionately used by sectors most strongly associated with unhealthy products. In 2024, outdoor advertising made up 30% of manufacturers' total food and drink advertising spend and 46% of out-of-Home (OOH) businesses' spend, compared with only 13% for supermarkets (figure 4). This imbalance matters because supermarkets typically offer a broad mix including many healthier items, whereas the OOH sector is dominated by higher-calorie food and drink, and as discussed below, a large share of manufacturers' advertised products are likely to be unhealthy.

Figure 4. Food and drink advertising spend by company type and media channel

2.2 Current outdoor restrictions underestimate children's exposure in public spaces and overlook adult health harms

Outdoor advertising was excluded from the recently introduced restrictions on the basis of proportionality, with the government arguing that intervention should focus solely on TV and online, where evidence shows children spend the majority of their time. The government's impact report concluded that the available evidence indicated banning outdoor less healthy food and drink advertising would not result in a justifiable reduction in childhood obesity. As a result, outdoor remains subject only to the existing CAP codes, which ban HFSS ads where under-16s make up more than 25% of the audience or within 100 metres of schools.

However, applying this child-audience test to a public space misses several crucial points and means the existing outdoor restrictions are insufficient. The '25% audience”' threshold ignores the absolute number of children exposed in busy areas simply because they are outnumbered by adults. And importantly, focusing advertising policy on protections to children alone overlooks the wider public health challenge: adults experience even higher rates of obesity than children.

2.3 Whilst local authorities have some control over outdoor advertising space, the scope and impact of this is limited

While many local authorities are adopting stronger outdoor advertising policies, they only have control over the assets they own; private sites remain outside their remit. Councils do not typically have data on privately owned advertising spaces in their area; however, in Bristol, it was estimated that only around 30% of advertising spaces are council-owned. A national policy covering all outdoor media is the only way to close this gap fully. There is clear evidence that this could be effective from the 2019 restrictions on the advertising of HFSS food and drinks across the entire Transport for London (TfL) network.

The fact that, since TfL's ban was introduced, at least 25 local authorities and two combined authorities[^8] have adopted similar healthier advertising policies across council-owned outdoor spaces is encouraging and demonstrates that local leaders have stepped up in the absence of national action. Commitments from almost all metro mayors to pursue similar approaches further highlight this momentum. However, relying on authority-by-authority action is inherently slow and inefficient, requiring hundreds of separate policy processes, each with potentially different interpretations and levels of ambition. With over 300 local authorities in England alone, comprehensive and consistent protections are likely to remain a distant reality without national restrictions.

Key point 3: Large proportions of food and drink advertising spend are focused on driving consumption of HFSS products, yet the government's current definition of less healthy food and drink excludes a significant proportion of products that are HFSS.

3.1 A large share of advertising spend is driven by unhealthy food and drink

Manufacturers and the out-of-home sector (including delivery apps) make up 72% (£1.7 billion) of all food and drink advertising spend relative to 24% (£550 million) by retail. This is disproportionate given that 88% of the calories we consume[^9] come from the retail sector. It matters because supermarkets sell a far broader mix of products - including many healthier options – whereas out-of-home businesses and manufacturers are far less likely to offer or promote healthier choices. For example, the out-of-home sector is dominated by higher-calorie items: at least 60% of meals sold in the sector exceed the recommended number of calories per meal.

The Nielsen dataset allows us to examine the type of products advertised by manufacturers and retailers in more detail than other sectors. Approximately 90% of manufacturers' food and drink advertising spend is focused on specific products and around 10% on brand advertising. Of manufacturers' product-focussed advertising spend, 61% was directed towards alcohol or products in one of the 13 food and drink categories in scope of the recent less healthy food and drink restrictions. By contrast, retailers spend approximately 37% of their food and drink advertising spend on product advertising and 63% on brand advertising. Of retailers' product-focused advertising, 53% of spend was directed towards alcohol or products in the 13 in-scope categories.

3.2 Product category exemptions risk missing a significant proportion of HFSS products

It has been argued that the current focus on only 13 food and drink categories defined by the UK government to be of most concern for childhood obesity does not go far enough. Under the current framework, a product would not be able to be advertised only if it exceeds the UK government's Nutrient Profiling Model (NPM) threshold for being considered HFSS, as well as falling within 1 of 13 specified food and drink categories and also being pre-packaged. (Please see part III for a discussion around the impact of the updated 2018 NPM recently committed to by the government).

Nesta's analysis of data from Worldpanel by Numerator's GB Take Home panel (over the period 1st January to 31st December 2024) shows that 41% of consumer spend in large supermarkets is on HFSS items based on the UK government's Nutrient Profiling Model. However, the 13 food and drink in scope categories capture only around 40% of this HFSS spend. This means that around 60% of spend on HFSS products falls outside of these categories, and thus outside the scope of advertising restrictions.[^10]

We recognise that any regulatory system which attempts to draw a binary distinction between 'healthy' and 'less healthy' foods faces difficult boundary decisions, including how to avoid capturing foods such as olive oil, Brazil nuts or unsweetened whole milk, which can exceed the Nutrient Profiling Model threshold but are generally considered part of a healthy diet. These considerations help explain why the current approach uses a limited set of legislative categories. However, this approach also creates clear anomalies, with products such as chocolate spread and toffee-coated nuts falling outside the thirteen categories despite being high in sugar and calories.

Key point 4: The brand exemption leaves 36% of food and drink advertising untouched by current regulations; the additional impact of range advertising is unknown and could further widen this gap.

The current version of advertising regulations permits all brands and ranges to be advertised, whether or not they contain unhealthy products.

Our analysis shows that 36% of food and drink advertising spend (£824 million) is already brand-focused and will therefore be untouched by current less healthy food and drink advertising restrictions.

Figure 5. Illustrative examples of brand and range advertising that may remain permitted under current restrictions

These UK campaigns illustrate how brand- or range-focused advertising could be interpreted as falling within this exemption, even where the underlying products fall under the UK government's definition of less healthy. Whether specific ads are permitted in practice depends on the interpretation by the ASA.[^11]

Walkers - Everyone has a favourite, 2025: Campaign across broadcast TV, video on-demand, social and OOH highlighting multiple crisp flavours in the range.

McDonald's - Happy Meal x Warner Bros, 2025: TV and online campaign promoting the Happy Meal range with movie tie-ins

Cadbury's - Made to Share, 2025: Campaign across broadcast TV, video on-demand, social and OOH promoting Dairy Milk sharing packs

While we discuss the evidence around the impact of brand advertising on consumption above, the evidence on the impact of range advertising specifically is effectively nonexistent. Furthermore, it is unclear how fully available datasets capture advertising that might be characterised as product 'ranges' according to the government's definition, meaning the true share falling outside scope due to the brand and range exemption could be higher than the stated figure (given it is unlikely that ranges are fully captured under the data definition of a brand). The brand and range exemption makes it likely that some product advertising spend will shift towards brand and range advertising. As a result, people may not see fewer ads from these companies, but different types of ads instead. For example, depending on the specific content and visuals used, advertising featuring McDonald's' golden arches or Cadbury's purple branding could be allowed, and it could even be interpreted under current definitions that the promotion of ranges such as Happy Meal or Dairy Milk would remain permissible on TV and online at any time (Figure 5). The boundaries between brand, range and product advertising are not always clear, and their interpretation ultimately rests with the regulator. This lack of clarity itself leaves open significant room for interpretation and potential circumvention.

Key point 5: Owned media is rapidly evolving and growing, but the scale and impact of this is unknown

The recent less healthy food and drink advertising regulations focus narrowly on 'paid-for' advertising, leaving company-owned channels, such as websites, organic social media (posts shared without paid promotion), and direct digital marketing (DDM) via email, SMS, or app notifications, largely unrestricted. This is the area of advertising which has likely seen the greatest evolution in the time since the regulations were initially announced eight years ago.

While the boundary between marketing and other public-facing company communications can be blurry, a particularly important gap is the exclusion of direct digital marketing, through which companies repeatedly target individuals with personalised messages designed to encourage food and drink purchases, often at the precise moment when a purchase is most likely. Unlike more visible channels, DDM operates behind the scenes, making it highly influential yet largely unexamined in public health research and policy with regard to scale and impact.

5.1 Direct digital marketing is widespread, growing and not covered by less healthy food and drink advertising rules

Direct digital marketing (DDM) is rapidly expanding and highly effective. The UK is the third largest sender of email marketing campaigns worldwide, launching around 830,000 annually, while SMS and push volumes are growing by 31% and 55% year-on-year, respectively. Despite being rated by marketers as the most effective digital channels, email, SMS and push communications sit outside the current less healthy food and drink advertising restrictions.

Despite this, almost all evidence on DDM comes from industry reports. While such studies consistently link repeated, targeted digital messages to higher engagement and more frequent food and drink purchases, there is almost no independent evidence on how many messages people actually receive, how exposure varies across population groups, or the impact of these channels on purchasing behaviour. This gap exists because messages are short-lived and tailored to individuals, not publicly visible, and increasingly automated, making it hard to measure exposure reliably.

To address this evidence gap, we tracked food and drink direct digital marketing using a multi-day diary study with a representative sample of over 1,500 adults.

5.2 Direct digital marketing routinely exposes adults to marketing designed to drive impulse purchases of unhealthy food and drink

Our research suggests that direct digital marketing for food and drink is a routine part of daily life for many adults. Nearly three-quarters (73%) of adults in the UK receive at least one such message each day, and around one in five (22%) receive three or more messages daily.

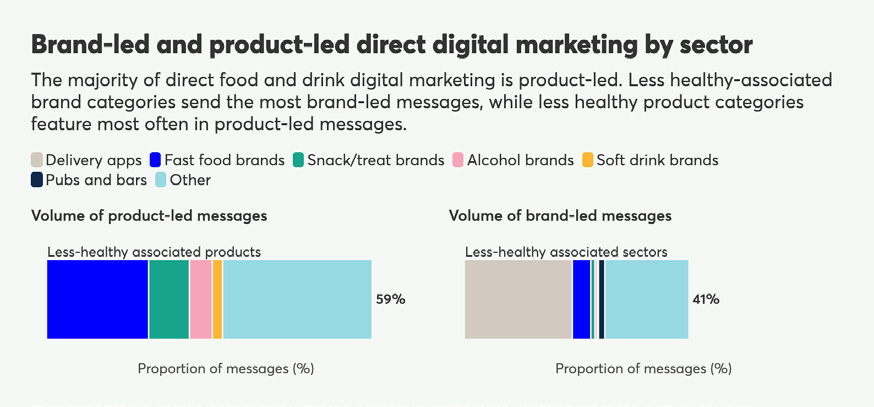

Nearly 60% of these messages promote specific food or drink products. Where messages promote specific products, more than half (54%) of these messages are promoting fast food, snacks and treats, alcohol or soft drinks – categories widely recognised in dietary guidelines as less healthy[^12] (figure 6).

Even when no product is shown, messages often promote brands closely tied to less healthy foods, potentially encouraging unhealthy food choices. When analysis is restricted to brand-led messages (ie, those that did not feature a specific product), 63% came from brands associated with less healthy food and drink categories. Taken together, 64% of DDM messages featured either an unhealthy product or came from a brand associated with less healthy food and drink categories.

Behavioural tactics reinforce this exposure and drive purchases. Over two out of five (40%) of food and drink DDM messages include urgency cues such as 'today only', while 70% promote discounts or multi-buy offers. These tactics are known to encourage impulse purchasing and can undermine efforts to support healthier choices.

Figure 6. Volume of brand-led and less healthy product-led direct digital marketing by sector

5.3 Younger and more deprived groups face higher exposure and more aggressive tactics

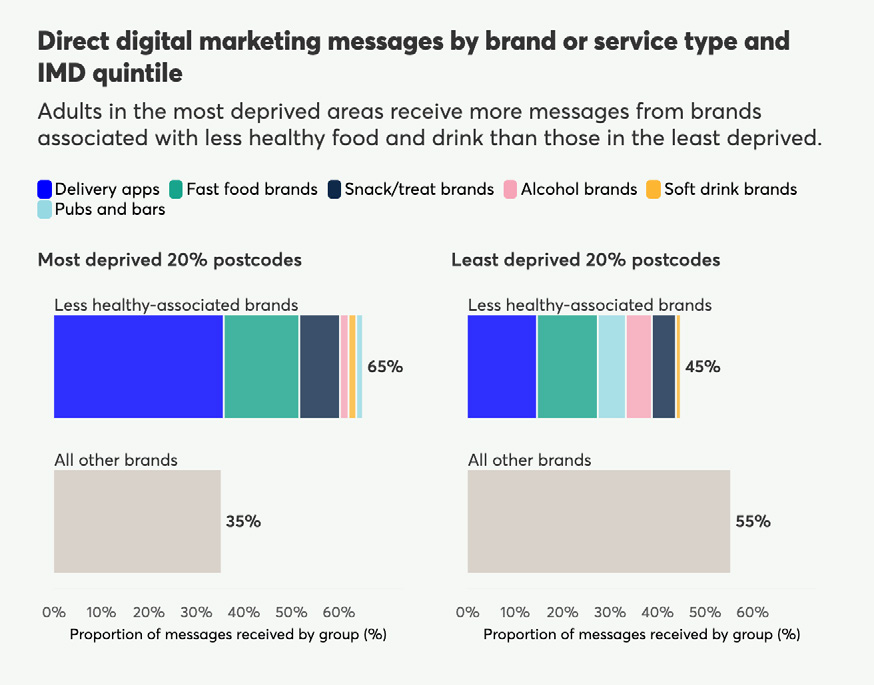

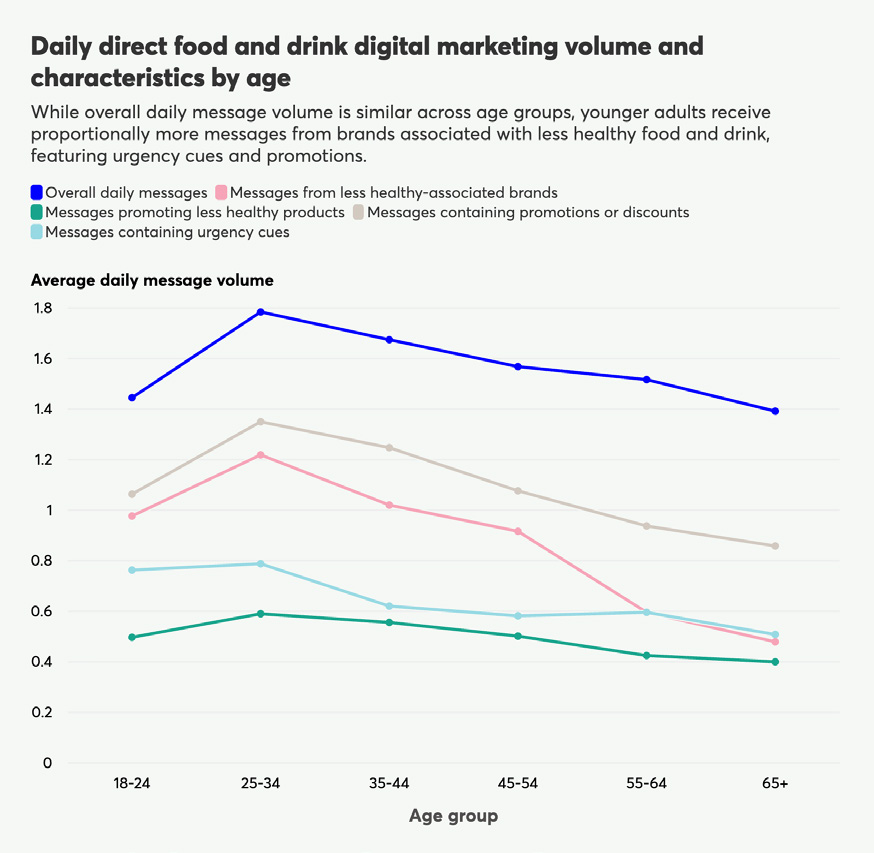

Our study suggests that food and drink DDM messages may be amplifying existing health inequalities. While the total number of food and drink DDM messages received was similar across areas, messages from less healthy brands were nearly 50% more common in the most deprived areas (65% of messages) than in the least deprived (45%). A similar, though less pronounced, pattern is observed when looking specifically at messages promoting less healthy products: 36% of messages received in the most deprived areas feature less healthy products, compared with 28% in the least deprived areas (figure 7). What's more, the proportion of messages received from less healthy brands is highest among adults under 35 years old and declines steadily with age, with the lowest levels observed among those aged 65 and over; with similar but less dramatic trends for messages for unhealthy products. This is notable because young adults aged 18-24 face the highest risk for weight gain.

Figure 7. Daily food and drink DDM volume and characteristics by age and IMD quintile

Daily direct food and drink digital marketing volume and characteristics by age

While overall daily message volume is similar across age groups, younger adults receive proportionally more messages from brands associated with less healthy food and drink, featuring urgency cues and promotions.

5.4 Fast-evolving AI and creator-led marketing are shifting food advertising into largely unregulated channels

These findings sit against the backdrop of a rapidly changing, technology-driven advertising industry; much of it shifting into channels that the new less healthy food and drink advertising rules do not cover. Experts we spoke to describe a sector being reshaped by AI, more personalised targeting, the growth of influencer networks, and mounting pressure to deliver quick, measurable results rather than long-term brand building. As one analyst put it, “This is the most change we've seen in 20–25 years".

Much of this change is happening through company-owned or lightly regulated channels outside current advertising restrictions. AI chatbots, like Chat GPT and Google Gemini, are beginning to act as "personal shoppers”, using personal data to generate highly targeted product suggestions. At the same time, brands are expanding large networks of 'micro-influencers' with modest but highly engaged audiences, offering products or small payments in return for content that feels personal and authentic, blurring the line between genuine recommendation and paid promotion; because this activity is spread across many individuals and often resembles personal posts rather than advertising, it is far harder to monitor or regulate.[^13]

Companies are simultaneously investing in targeted marketing via apps, email, SMS and social platforms, fuelled by the growing volume of consumer data these channels collect and the use of AI to analyse it. Together, these trends create a volume and complexity of food and drink promotion that moves faster than regulation. For unhealthy food and drink, the risk is that some of the fastest-growing marketing channels are precisely those the HFSS rules don't touch.

The growth in this sector highlights how the development of the current regulations has failed to keep up with a rapidly evolving industry. Whilst banning all paid-for activity would seem like a blunt instrument, the current approach errs too far in the opposite direction. Although consumers technically opt in to direct marketing and can unsubscribe at any time, this does nothing to protect children from exposure and our research suggests that people often subscribe because opting out is difficult.[^14]

One option would be to set basic safeguards for direct and company-owned channels used to promote HFSS products, such as simple age checks on webpages of brands associated with unhealthy products and when people sign up and for direct messages. This would still allow companies to communicate with customers while reducing unintentional access to unhealthy food marketing, particularly for children. Alternative options could include absolute limits on messages and making opt-out an easier process.

Part III - Implications for current and future policy

Despite the recent implementation of new regulations, the UK's less healthy food and drink advertising rules still reflect a system built for an earlier age. The initial intent behind the regulations that have come into force was laudable, but the output which is in force today is much less impactful than it could be. The exemption of advertisements for brands and ranges, the narrow focus on pre-watershed TV and online, and the lack of regulation for owned and direct marketing mean companies can continue to promote unhealthy food and drink across much of the advertising landscape.

Our analysis has shown how advertising policy struggles to keep pace with rapid shifts in advertising spend and technology. As marketing moves fluidly between formats, policies tied to specific media channels risk displacement. To make future policy watertight, it needs to do more than comprehensively close individual loopholes. We need an approach to advertising policy that shapes the entire marketing environment and is adaptable, ensuring policy evolves alongside innovation.

Our Blueprint shows what could be achieved with a far more ambitious approach to advertising policy. A package including a 21:00–05:30 watershed for TV and online advertising, tight limits on online paid advertising, and a ban on less healthy advertising across public transport, including bus stops, train stations, and tube stations, could reduce children's daily calorie intake by around 44 kcals, leading to a 16% relative reduction in obesity prevalence over five years. This is in stark contrast to the impact assessment by the UK government, which suggests that the current restrictions will reduce daily calorie intake of children by around 2.10 kcal[^15]; implying an obesity reduction impact of less than 1%.

Key point 1: We estimate that current restrictions cover just 8% of food and drink advertising spend, and once displacement to unrestricted channels and brand-focused advertising is accounted for, they are likely to affect only around 1% of food and drink advertising spend.

Drawing on the findings in this report, we estimate that around 8% of 2024 food and drink advertising spend is in scope of the current restrictions. However, companies are likely to redirect a substantial share of affected spend into brand and range advertising or into unrestricted media channels. When these likely adjustments are taken into account, we estimate the regulations will affect only around 1% (£20 million) of total food and drink advertising spend. That is roughly the annual food and drink advertising budget of a single company like Domino's Pizza. It remains unclear whether this spend will be redirected towards healthier products, shifted into other forms of marketing, or absorbed elsewhere. However, we estimate that, in practice, the regulations will prevent only around 3% of spend on HFSS products within the in-scope categories.[^16]

As detailed in Appendix 1, our estimates exclude advertising in media channels not covered by the policy (such as post-watershed TV, outdoor and radio) and types of advertising not covered by the policy (such as brand and range advertising). They also exclude products that are not in scope of the legislation, either because they fall outside the 13 specified food and drink categories despite being HFSS, or because they are not defined as HFSS according to the UK government's NPM threshold.

Key point 2: We estimate that closing the loopholes which currently exist could lead to 33% of food and drink advertising spend being in scope of regulations.

We recommend three pragmatic updates to the current restrictions, which would go some way to improving impact.

- Expand advertising restrictions to outdoor spaces: as detailed above spend on outdoor advertising has risen significantly since the current restrictions were announced and this is the most likely channel that advertising will be displaced into. Second, the scope for local government intervention is limited, highly resource-intensive and likely to take a long time.

- Introduce restrictions on advertising for unhealthy brands and product ranges, alongside product-level restrictions.

- Redefine the products in scope so that all[^17] HFSS products are covered, rather than only those within the current 13 categories.

The government should assess the scale and impact of non-paid-for advertising and consider introducing appropriate policy safeguards.

Of these updates, introducing restrictions on advertising for unhealthy brands and product ranges is likely to be particularly important. Our analysis shows that over a third of food and drink advertising spend is already brand-focused and therefore entirely untouched by current rules. While defining what constitutes an 'unhealthy brand' is more complex than classifying individual products, this challenge should not be a reason for inaction. Practical options exist: for example, permitting advertising only where a healthier product is featured (comparable to the approach taken in Abu Dhabi), or allowing brand and range advertising only where a brand is not 'synonymous' with an HFSS product or where the majority of products in a range are not HFSS (an approach previously set out in ASA codes of practice, which are separate and predate the recent less healthy food and drink advertising regulations).

When accounting for the various limitations and exemptions in place with the current regulations, we estimate that current regulations will affect only 1% of total food and drink advertising spend once businesses adapt. However, as detailed in Appendix 1, closing these loopholes and expanding the regulations to other food and drink categories could bring up to 33% of total food and drink advertising spend into scope (including alcohol advertising, or around 30% if alcohol is excluded).[^18]

Closing these loopholes would strengthen the impact of existing restrictions by limiting companies' ability to shift spending into exempt channels or formats, and encouraging greater promotion of healthier food and drink.

The initial intent of the current restrictions was positive, but the outcome is likely to be far less impactful than it could have been. Our estimates suggest that the proportion of food and drink advertising spend in the scope of the regulations is around four times smaller than it could be under a more comprehensive approach.

While governments must rightly balance public and commercial considerations, the current restrictions appear overly weighted towards the latter. The government's recently announced moonshot to end the obesity epidemic, signals a step change in ambition and approach. Shaping the advertising sector should be a central, and currently under-tapped, part of delivering that ambition.

Key point 3: The government should take and implement lessons from the policy development of the current advertising restrictions.

In part 1, we described the timelines and process taken to implement the current restrictions. The outcome has been a significant delay and reduction in the potential impact this policy could have. The healthy food standard, consisting of mandatory reporting and health targets for large food businesses, has the potential for a huge population impact at a time of crisis in respect of obesity prevalence. It is crucial that this policy is implemented as quickly and impactfully as possible. To this end, we would recommend the following in regard to the process the government takes to implement the policy:

- Set the implementation timeline in legislation, including the dates that requirements and enforcement actions will take effect, and stick to it. This will give businesses certainty and avoid delays that jeopardise policy impact. Returning with further legislation to amend dates, as happened with the recent advertising regulations, should not be an option.

- Adopt a risk-based approach to industry engagement that recognises the food industry's vital role in feeding the nation and in operationalising the policy. To formalise policy stewardship, the government should have robust and transparent mechanisms for accountability and to safeguard against undue industry influence:

- An independent advisory panel with a balance of sector representation should serve as a central clearing house for engagement on the Healthy Food Standard. Here, the food industry's perspectives could be explicitly balanced by the evidence-based scrutiny of academics, health professionals, and advocacy groups. This would ensure industry influence is visible, challenged, and managed within a public-health-first framework.

- Establish an immediate 'open book' framework for the Healthy Food Standard while legislating for long-term reform. Current mechanisms track some formal industry engagement, but miss the covert lobbying that historically delays public health measures. To secure the integrity of the policy now, the government should voluntarily exceed current statutory requirements by disclosing all industry interactions and encouraging industry disclosure of their research ties. Concurrently, a permanent legislative framework for public health policy should be drafted, modelled on the robust scope of Irish, Chilean and French rules, and permanently align UK transparency with international best practice.

- Ensure commitment to the original public health policy objective throughout implementation to prevent watering down and prioritisation of industry interests over health impacts. DHSC should retain authority over definitions and exemptions for any policy where public health is the primary statutory objective.

Key point 4: The new government Nutrient Profiling Model (NPM) will increase the impact of both current advertising regulations and the healthy food standard. However, given the potential oversized impact of the healthy food standard, applying the new NPM to policy must not delay the healthy food standard's implementation.

The analysis presented in this paper is based on classifying foods as HFSS or not based on the UK government's 2004 to 2005 Nutrient Profiling Model (NPM), which currently underpins advertising restrictions. However, it is important to note that the UK government has recently published a long-awaited update to the NPM.

The updated model, called the Nutrient Profiling Model 2018, reflects the latest scientific understanding of diet and health and represents a substantial improvement. Government analysis suggests that applying the updated model to existing advertising and promotion restrictions could increase the per-person per-day calorie reduction of the policies by up to 30%. We welcome this update.

However, last year the government announced the Healthy Food Standard, which presents an opportunity to use the NPM in a far more ambitious and impactful way.[^19] This policy will require large food businesses to meet mandatory targets to improve the healthiness of their sales. Achieving mandatory health targets would give businesses the flexibility to use any tools at their disposal to improve the healthiness of their entire product range. This broad change in our food environment could help around 3 million people achieve a healthier weight. Based on the government's impact statement, mandatory targets could have at least a two-fold higher impact compared to implementing the updated NPM (the updated NPM would, in fact, make the healthy food standard even more impactful).

With so much at stake - the health of our nation, the NHS and our economy - applying the new NPM to policy must therefore not delay the implementation of the healthy food standard. At Nesta, we think the government should use this parliament to establish powers for mandatory data reporting (which could be used to monitor the effectiveness of advertising regulations), mandatory targets and enforcement mechanisms, laying the groundwork for the healthy food standard to deliver on its full potential.

How could the government make the restrictions more watertight?

Here we seek to enumerate the potential coverage of expanded regulations. The government could work to close several of the loopholes that we have outlined above:

- Expand restrictions to include brand-focused advertising

- Expand restrictions to include outdoor advertising

- Expand coverage beyond the current 13 legislative food and drink categories to all HFSS products (according to the UK government's NPM threshold).[^25]

Option 1: Expand to unhealthy brand-focused advertising.

We estimated the increased spend covered if the government were to expand advertising restrictions to also include advertising for unhealthy brands, even when a specific unhealthy product is not featured. This would require discussion between the government and food companies to determine what should count as an unhealthy brand.

In the absence of a pre-existing government definition, we have explored multiple approaches to try to define unhealthy brands in the data we have available. However, we are unable to reach a satisfactory level of precision. For example, we could assume the proportion of unhealthy brand advertising is the same as the proportion of unhealthy product advertising; however, data for some sectors (eg, OOH) did not give us a granular enough breakdown of food categories advertised to identify unhealthy product ad spend.

We have therefore tentatively assumed that 'less healthy' brand-focused ad spend would be equivalent to the proportion of revenue retailers derive from HFSS products in large grocery retailers in data from Worldpanel by Numerator's GB Take Home panel over the period 1st January to 31st December 2024 (hereon referred to as 'Worldpanel data'). We use revenue rather than the kcal share of HFSS products because, in the absence of more detailed data, the most reasonable assumption is that companies spend more on advertising the products that generate the highest revenue. Based on this, we estimate that 41% of brand-focused advertising would be classified as unhealthy—a plausible figure given it is close to estimates from Cancer Research UK, which found that around 48% of TV adverts in 2019 promoted HFSS products.

In 2024, £400 million was spent on brand-focused food and drink advertising on pre-watershed TV and online. Based on the assumption that 41% of this spend was for 'unhealthy' brands, we estimate that extending the current less healthy food and drink advertising regulations to cover unhealthy brand advertising would cover an additional ~£170 million of ad spend.

When combined with the existing January regulations, this would total ~£360 million, or 16% of total ad spend.

Option 2: Expand to include brand-focused and outdoor advertising

For product-specific advertising, we use the same method as with pre-watershed TV and online ads to estimate the outdoor unhealthy advertising spend. Product advertising is restricted to only those featured in the 13 legislative categories (£230 million), under the previous assumption that 54% of spend would be on HFSS from the Worldpanel data, and outdoor less healthy product-focused advertising is estimated to come to £130 million.

Total outdoor brand-focused food and drink advertising spend (£190 million) is multiplied by the 41% HFSS share (as in Option 1), giving an estimated £79 million of HFSS brand-focused outdoor advertising.

Together, expanding to outdoor advertising covers an additional ~£210 million.

When combined with the regulations introduced in January 2026 and option 1, this policy would cover ~£560 million of advertising spend - or 24% of total spend.

Option 3: Expand to include brand-focused, outdoor advertising, and expand the definition for less healthy to include all products with an unhealthy NPM score.

Based on our analysis of Worldpanel data, 54% of the spend from the 13 legislative categories is unhealthy based on the government's NPM threshold, meanwhile 35% of spend on all products not in the 13 categories is unhealthy according to the NPM.

To estimate the coverage of this policy, we assume that advertising spend is proportional to consumer spend (ie, the percentage of spend on ads for HFSS products matches the percentage of spend on HFSS products). Using this logic, we multiply the spend for products within the 13 regulated categories by 54%, while for products falling outside those 13 categories, including alcohol, we multiply the spend by 35% to capture the remaining unhealthy balance. This calculation is applied across pre-watershed TV, online, and outdoor advertising platforms.

Expanding product advertising to cover all advertisements with an unhealthy NPM is estimated to cover an additional £190 million.

Overall, when combined with previous options, this policy would cover £760 million, 33% of total food and drink advertising spend. If we were not to include alcohol, this policy option would cover £700 million (30%) of total food and drink advertising spend.

The table on the next page shows the breakdown of each of the three options.[^26]

| Option | Media scope | Ad category | Additional spend covered | Cumulative total | Proportion of total food and drink ad spend |

|---|---|---|---|---|---|

| January 26 regulations | Pre-watershed TV and online | Product ads within the legislative categories | £190 million | £190 million | 8.3% |

| Option 1 | Pre-watershed TV and online | Brand-focused | £170 million | £360 million | 16% |

| Option 2 | Outdoor | Product ads within the legislative categories | £130 million | -- | -- |

| Brand-focused | £79 million | £560 million | 24% | ||

| Option 3 | Pre-watershed TV, online and outdoor | Product ads not within the legislative categories | £190 million | £750 million | 33% |

Appendix 1: Method to investigate the proportion of ad spend covered by recent advertising legislation

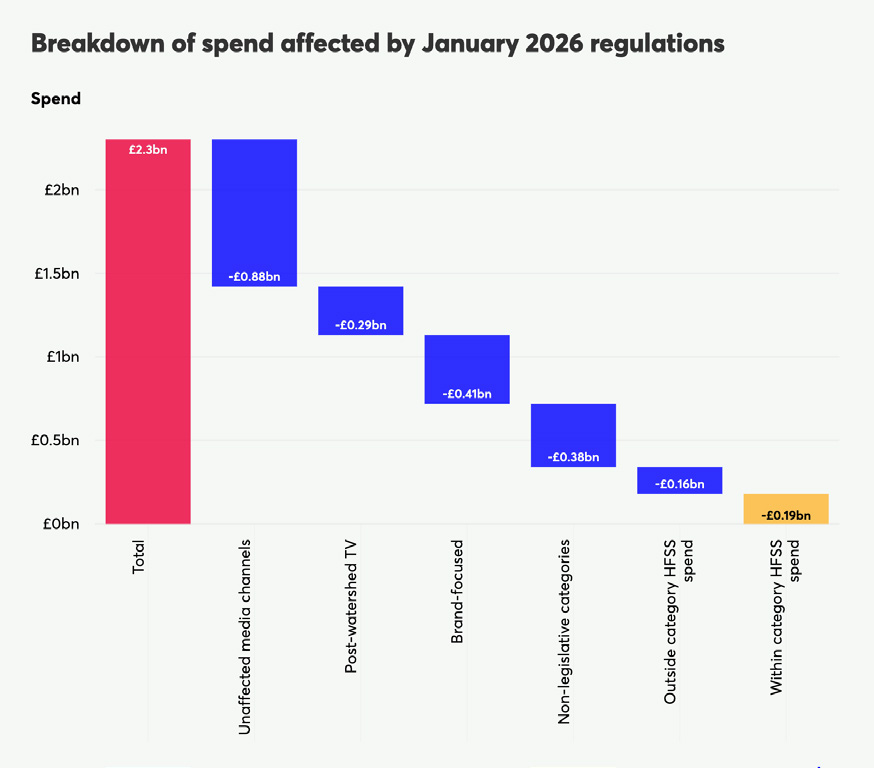

We have used Nielsen's Ad Intel data to estimate what proportion of ad spend would be covered by existing legislation. The legislation covers advertisements in specific channels (digital, social and pre-watershed TV), product-specific (as opposed to brand-focused adverts), and for foods in specific legislative categories.[^20] In the 2024 Nielsen dataset, this represented £360 million or 15% of total ad spend.

To arrive at our final figure, we make an additional assumption about the share of advertising spend within the 13 legislative food and drink categories that is for HFSS products. Nielsen Ad Intel does not report HFSS status, so we proxy this using consumer purchasing data. Specifically, we draw on analysis of data from Worldpanel by Numerator's GB Take Home panel (over the period 1st January to 31st December 2024), which shows that 54% of consumer spend within these 13 categories is on products classified as HFSS under UK government NPM thresholds. (This 54% figure relates only to products within the 13 in-scope categories. It is distinct from the earlier 41% estimate, which reflects the proportion of total consumer food and drink spend that is on HFSS products across all categories.) Applying the 54% figure to the total ad spend, we estimate that total spend covered by current legislation is £190 million or 8% of the total.

The table on the next page breaks down the 2024 Nielsen ad spend to estimate the total spend on advertising covered within existing legislation.

| Description | Total spend | Share of total |

|---|---|---|

| Total ad spend Filtered for food and drink advertising, all 2024 | £2.3 billion[^21] | 100.00% |

| Unaffected media channels Filtered for advertising media channels not affected by regulation | £880 million | 38.22% |

| Affected media channels Filtered for only TV, social and digital advertising | £1.4 billion | 61.78% |

| Post-watershed TV TV advertisements shown between 9:00pm and 5:30am | £290 million | 12.39% |

| Pre-watershed TV and digital and social All social and digital, and TV advertisements filtered for all after 5:30am and before 9pm | £1.1 billion | 49.39% |

| Brand-building, pre-watershed and online Filtered for where an advertisement has been flagged as brand ads | £410 million | 17.79% |

| Product advertising, pre-watershed and online Filtered for all ads not identified as brand ads | £730 million | 31.60% |

| Non-legislative categories, pre-watershed and online product ads Filtered for all advertisement types not covered in the identified 13 categories by the government | £380 million | 16.25% |

| Legislative categories, pre-watershed and online product ads Filtered for advertisement types identified within the 13 government categories | £360 million | 15.35% |

| Within category HFSS spend Adjusted for assumed share of ad spend on HFSS products within legislative categories[^22] | £190 million | 8.30% |

| Outside category HFSS spend Remaining adjusted ad spend | £160 million | 7.05% |

Figure 8: Waterfall chart showing the breakdown of total food and drink advertising spend and what the January 2026 regulations cover[^23]

Limitations and notes

Advertisements have been filtered to ensure they are relevant food and drink advertisements using the lowest level of description available through the dataset, but there may be some overlap for broader categorisation.

The total digital and social spend figures are likely an underestimate as Nielsen's capture of these channels is not 100% complete.

For categorising whether an ad is within the 13 government categories, spend has been matched using the most detailed ad description given. However, certain sectors, such as out-of-home and delivery apps, use broader definitions, so they do not split out much. This means that it is likely that for these sectors, our estimates of the proportion of products within the 13 categories will be a slight overestimate. Neither category makes up a majority of the dataset.

How will advertisers respond?

If brands wish to continue promoting unhealthy product sales, they are expected to pivot rather than cancel their campaigns and reduce spend completely. We anticipate two primary reactions:

- Shift to brand advertising: We make a tentative (due to a lack of evidence) assumption that approximately 50% of spend on unhealthy products affected by January 2026 regulations transition into brand-led campaigns (which are exempt from the restrictions). We estimate that brand advertising spend on pre-watershed TV and online will increase by £95 million, leaving the total spend covered by the regulations as £95 million.

- Media channel displacement: The UK government's impact assessment estimates that 79% of restricted ad spend will be displaced to other non-regulated channels (such as outdoor), with only 21% of the spend being truly "lost." Using the government's estimates, we estimate that £75 million of TV and online food and drink advertising will be displaced to other channels.[^24]

When factoring in these displacement and pivot strategies, the real-world impact on advertising volume is minimal. We estimate the regulations will, in fact, impact only £20 million per year of food and drink advertisements - 1% of total food and drink ad spend.

Within total food and drink ad spend, we estimate that £670 million is currently spent on advertising HFSS products within the 13 in scope categories. We estimate that only around £20 million of this will be directly prevented by the regulations – equivalent to around 3% of HFSS advertising spend in these categories.

Endnotes