The breadth of the Warm Homes Plan reflects the major challenges it is trying to solve: reducing energy bills, reducing fuel poverty, and reducing emissions from homes.

The Department for Energy Security and Net Zero (DESNZ) has responded to these challenges by setting new delivery targets:

- grow heat pump supply chains to deliver 450,000 installations in 2030

- install solar panels on three million homes over the next four years

- upgrade five million homes by 2030

This analysis digs into the detail behind those targets and considers how and whether they will be fulfilled. Ultimately, we find that DESNZ makes a good case that the Warm Homes Plan can deliver its ambitions; but sticking the landing will not be easy.

Even with its generous £15 billion funding settlement, the Warm Homes Plan has created many mouths to feed. Heat pumps and solar panels in particular are going to account for the majority of the plan’s budget, and may end up competing for the limited resources of schemes such as the Warm Homes Investment Fund. There are also risks that are hard for DESNZ to control, such as energy prices, or the capacity of local authorities. DESNZ is not blind to these, and the plan outlines what they will do to mitigate those. But nonetheless, the targets set out in the plan leave little room for error.

By Marcus Shepheard and Daniel Lewis

The breadth of the Warm Homes Plan reflects the major challenges it is trying to solve: reducing energy bills, reducing fuel poverty, and reducing emissions from homes. The Department for Energy Security and Net Zero (DESNZ) has responded to these challenges by setting new delivery targets:

- grow heat pump supply chains to deliver 450,000 installations in 2030

- install solar panels on three million homes over the next four years

- upgrade five million homes by 2030

This analysis digs into the detail behind those targets and considers how and whether they will be fulfilled. Ultimately, we find that DESNZ makes a good case that the Warm Homes Plan can deliver its ambitions; but sticking the landing will not be easy.

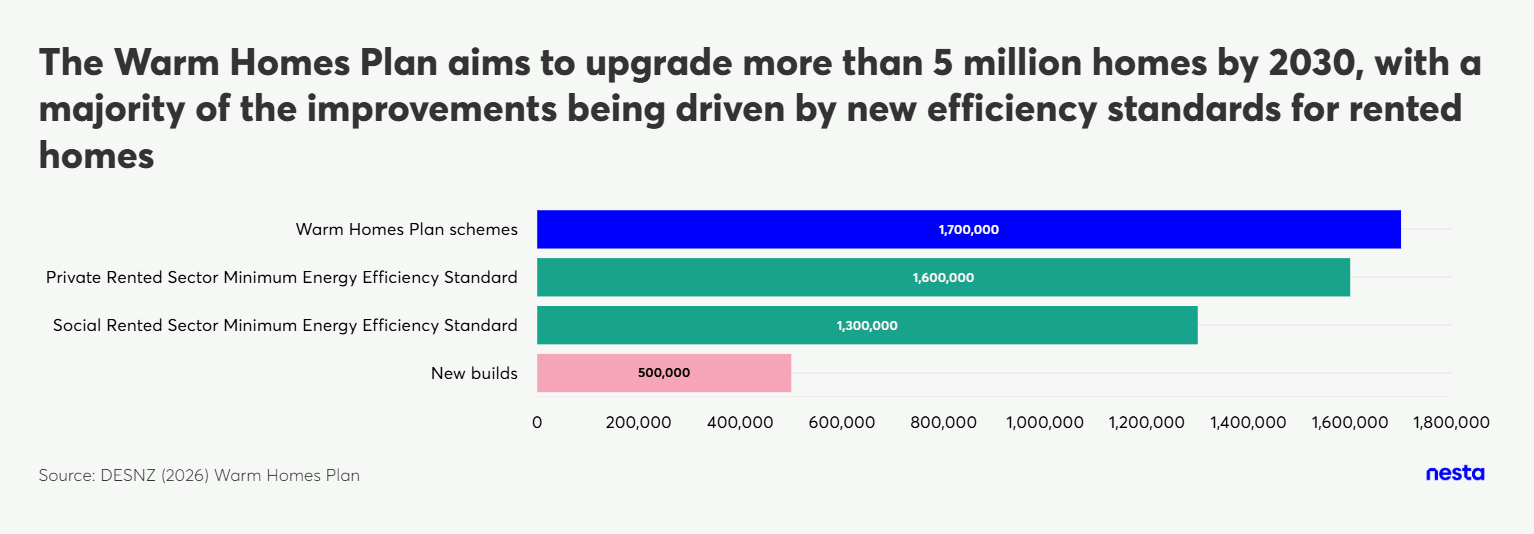

The Warm Homes Plan aims to upgrade more than 5 million homes by 2030, with a majority of the improvements being driven by new efficiency standards for rented homes

Figure 1 - Measures included within Warm Homes Plan commitment to improve five million homes

Even with its generous £15 billion funding settlement, the Warm Homes Plan has created many mouths to feed. Heat pumps and solar panels in particular are going to account for the majority of the plan's budget, and may end up competing for the limited resources of schemes such as the Warm Homes Investment Fund. There are also risks that are hard for

DESNZ to control, such as energy prices, or the capacity of local authorities. DESNZ is not blind to these, and the plan outlines what they will do to mitigate those. But nonetheless, the targets set out in the plan leave little room for error.

For further information on the other key policies included in the Warm Homes Plan, please refer to Nesta's initial response.

1. Reaching 450,000 heat pumps a year by 2030 requires contributions from all schemes

Heat pumps are the key technology to decarbonise home heating. In the Seventh Carbon Budget's Balanced Pathway, the Climate Change Committee envisages that 77% of existing UK homes will use a heat pump by 2050.

The UK's heat pump market is growing quickly, faster than other European countries, and much of this has been driven by support from government schemes. The UK government wants to grow the heat pump market to deliver 450,000 installations a year in 2030. This is a step back from the older target of 600,000 installations per year by 2028, reflecting the fact that recent progress has been slower than hoped.

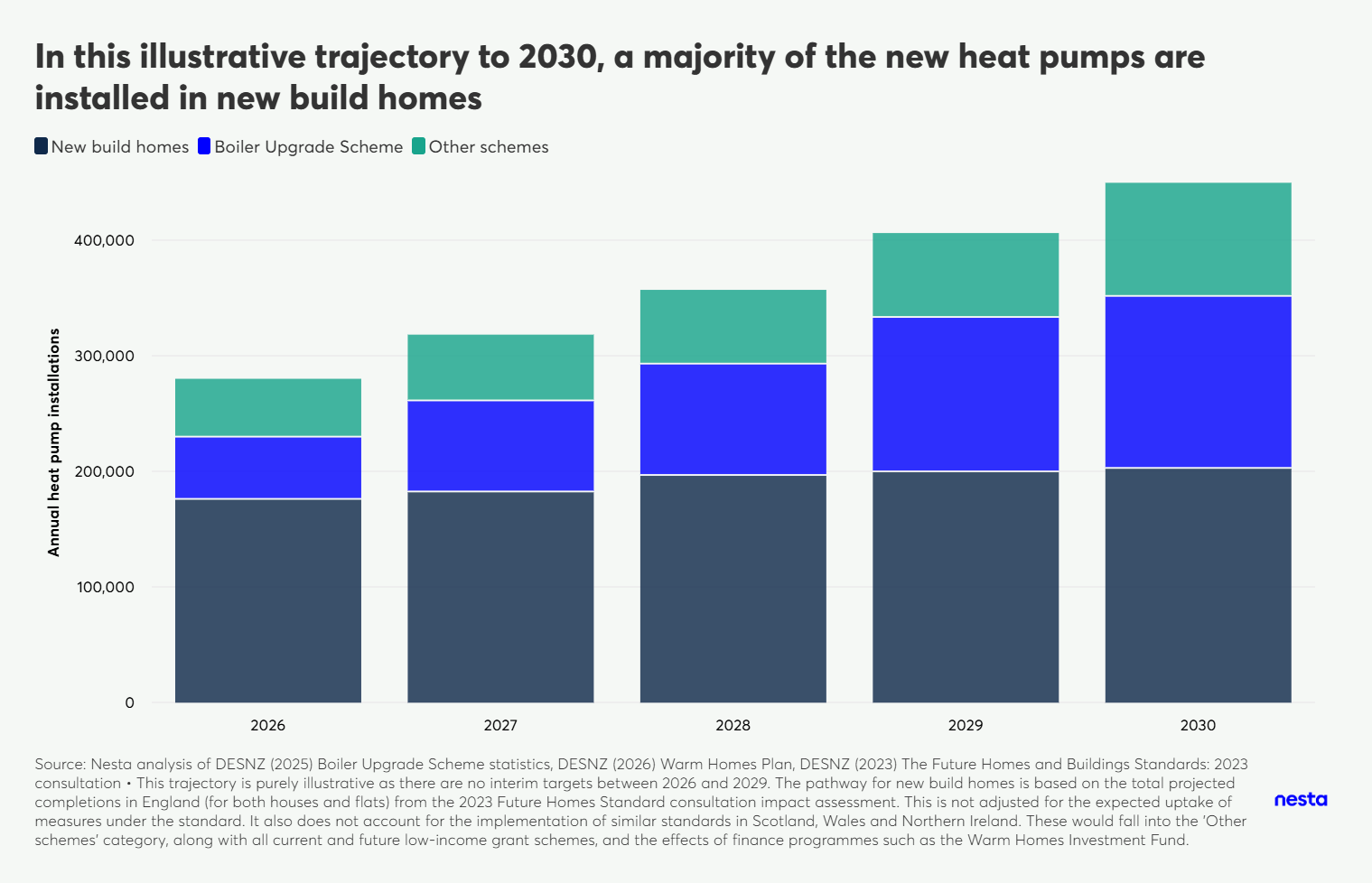

In this illustrative trajectory to 2030, a majority of the new heat pumps are installed in new build homes

Figure 2 - Estimated annual trajectory of heat pump installations up to 2030

Of the 450,000 headline target, DESNZ expects that 200,000 heat pumps will be installed in new homes in England in 2030, thanks to the Future Homes Standard (and other reforms).1 It is unclear whether this also includes new homes with heat pumps as a result of similar standards in Scotland, Wales and Northern Ireland (none of which are more advanced than the Future Homes Standard for England right now).

Our analysis suggests that the Boiler Upgrade Scheme could deliver up to 150,000 heat pumps in England and Wales in 2030 (if it gets continued funding through 2030/31). The remaining 100,000 or more heat pumps will come from the low-income schemes, the consumer loan, or projects supported by the £2.7 billion Warm Homes Investment Fund. Other grant schemes and regulations in Scotland, Wales and Northern Ireland will also play a part.

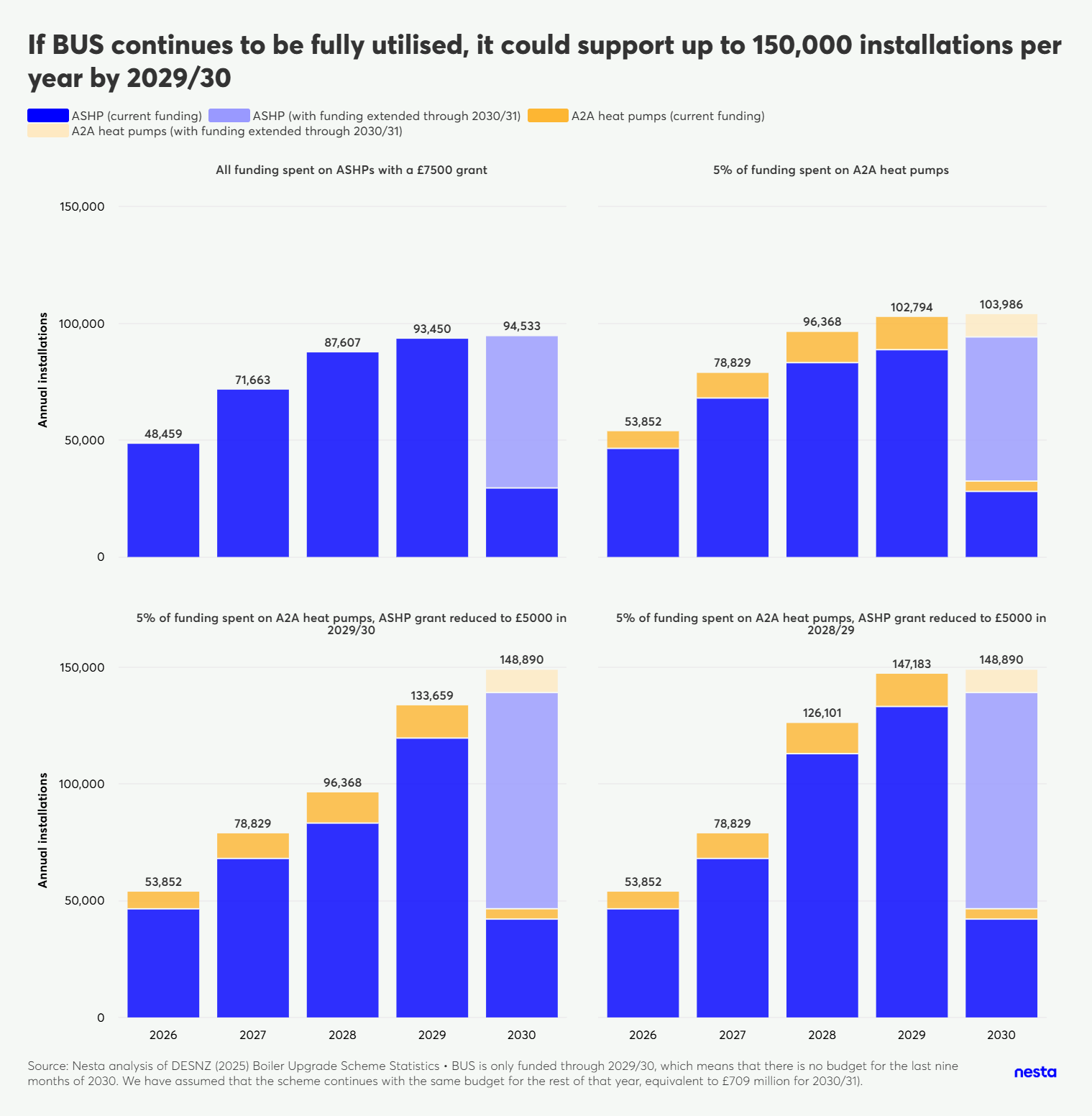

The Boiler Upgrade Scheme could support over 150,000 heat pump installations a year within four years, but hitting the 2030 target depends on it getting further funding

The Boiler Upgrade Scheme (BUS) is a major engine of the heat transition, and has supported over 72,000 heat pump installations since it launched, with uptake growing by 30% year on year. Its budget is due to increase by 26% per year on average over the next four years, in line with this rising demand.

Hitting the UK government's 2030 target depends a lot on whether BUS gets funded through the 2030/31 financial year. Currently, BUS only has funding for the first three months of 2030. If demand for the scheme continues to grow, and funding remains fully utilised, BUS could support over 150,000 heat pumps per year by 2029/30. But without an extension, BUS would only deliver 29,500 to 46,500 heat pumps in the actual target year, as it would only run until March 2030. This represents a potential shortfall of 65,000 to 102,000 heat pumps against the target of 450,000. It seems unlikely that this amount can be made up from other sources.

If BUS continues to be fully utilised, it could support up to 150,000 installations per year by 2029/30

Figure 3 - Projected heat pump installations via BUS to 2030

BUS used all of its funding in 2024/25, and is on track to use over 90% of this year's budget. We expect that future allocations rising in line with demand could be fully utilised.

-

If all of BUS's future funding is utilised for heat pumps (with a £7,500 grant), it would deliver 29,500 heat pumps in 2030. Or up to 94,500 heat pumps if it is funded through 2030/31 (395,000 over five years).

-

BUS will also cover air-to-air heat pumps (A2A) from April. As these are cheaper than other types of heat pump - with a smaller £2,500 grant - the scheme can offer more for the same budget. If A2A grants account for 5% of the BUS budget going forwards then the scheme would deliver 32,500 in 2030, or up to 104,000 heat pumps with funding through 2030/31 (436,000 over five years).

The cost to install an air source heat pump has fallen by 11% in real terms since 2022. If this trend continues then it will fall below £10,000 by late 2028, although this depends on heat pumps keeping a zero-rate of VAT beyond 2027. At some point the UK government may be justified in reducing the BUS grant, as it did for electric cars in the past. This could reduce demand, but would make the scheme's budget go further.

- Reducing the main heat pump grant to £5,000 in 2029/30 (alongside spending 5% of the scheme on A2A) would increase the potential number of heat pumps installed in 2030 to 46,500. This rises to 149,000 if BUS is funded through 2030/31 (512,000 over five years, or 555,000 if the grant is reduced in 2028/29).

Depending on whether BUS gets funded in 2030/31, another 100,000 to 200,000 retrofit heat pumps will need to come from other schemes

After new builds and BUS, DESNZ still needs to deliver a further 100,000 to 200,000 heat pumps in 2030 to reach its target. These will need to come from other places such as schemes targeting low-income households; those run by the devolved governments in Scotland, Wales or Northern Ireland; or potentially from new financing schemes such as the consumer loan scheme or the Warm Homes Investment Fund.

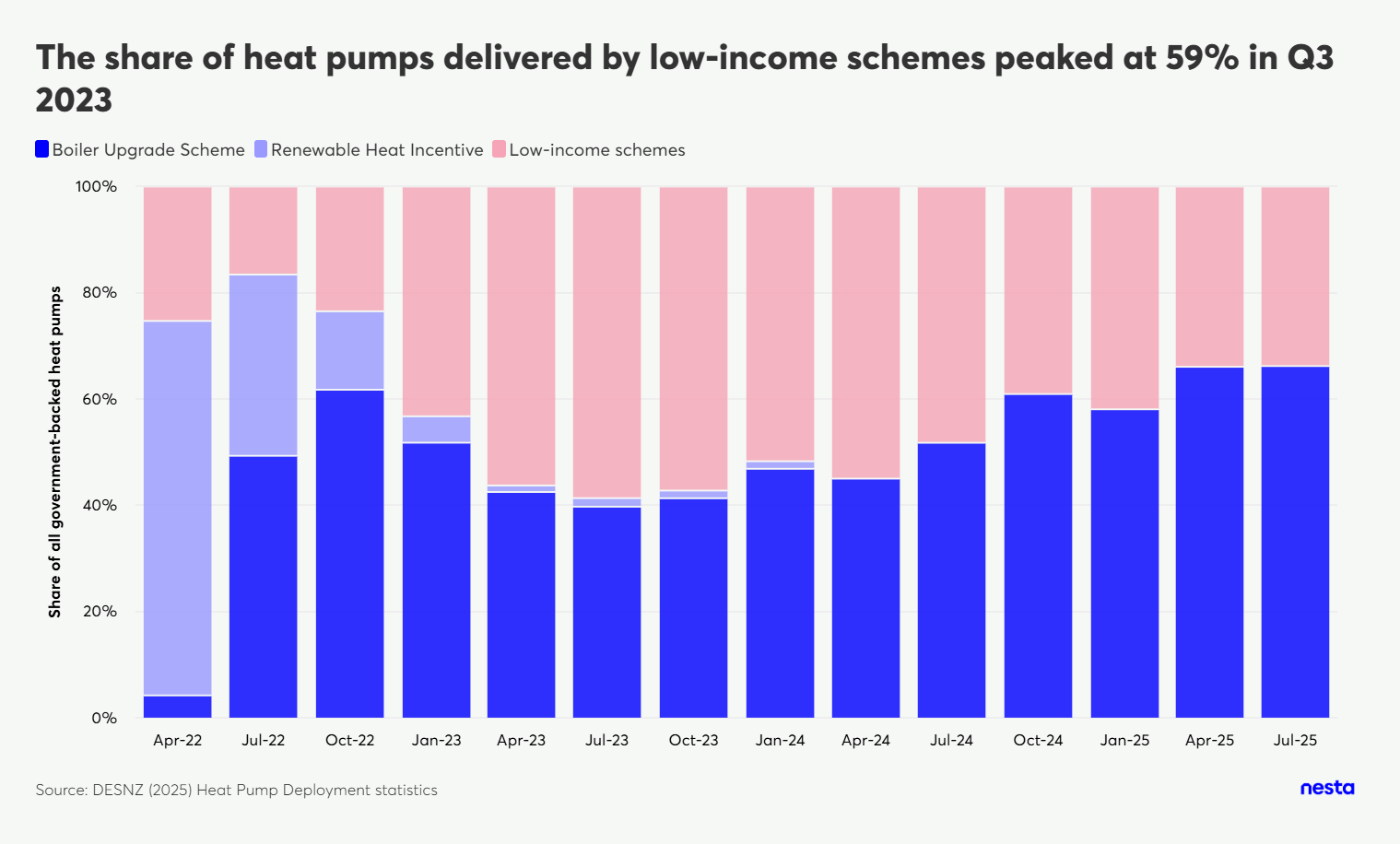

The share of heat pumps delivered by low-income schemes peaked at 59% in Q3 2023

Figure 4 - Heat pump deployment via UK government programmes

Since April 2022 the UK government's low-income schemes have supported 43% of the retrofit heat pumps installed in the UK - however their contribution is falling. The problem here is that 81% of these heat pumps were delivered through the Energy Company Obligation (ECO), which will end this year, and 8% through the Home Upgrade Grant (HUG), which ended in 2025. The remaining low-income schemes (the Warm Homes Local Grant and the Warm Homes Social Housing Fund) are not designed to install many heat pumps, but will not be replaced by the new integrated scheme until 2028.

DESNZ is going to consult on the design of this new scheme which should shift focus to electrification. This would mean more heat pumps being installed from 2028. But even growing the new scheme to match the 20,000 heat pumps per year that ECO currently delivers will take effort. Getting to 100,000 (or more) will be a significant challenge.

DESNZ is applying £5 billion of Financial Transactions (and £300 million of other capital budgets) to several new schemes including a £2 billion consumer loan scheme, and a £2.7 billion Warm Homes Investment Fund.

We expect that some households will use low-interest consumer loans to bridge the gap between the BUS grant and the total cost of a heat pump. But it seems unlikely that anyone will choose to finance a heat pump and forego the BUS grant. As such, these loans are unlikely to increase the total number of heat pumps above what is accounted for by BUS's budget. However, if the growing availability of cheap finance, alongside falling installation costs, prompts DESNZ to reduce the size of the BUS grant, this would increase the number of heat pumps that could be delivered.

The Warm Homes Investment Fund has the potential to be a new source of additional heat pumps above and beyond the existing schemes. DESNZ envisions some of this money being used to stand up area-based schemes delivered by local authorities or housing associations. However, the extent to which this will be achieved remains to be seen. DESNZ needs to do a lot of work to create scalable delivery models that can get this money out the door.

Ultimately, it is uncertain how DESNZ will deliver the remaining 100,000 heat pumps per year by 2030. We expect that the new low-income scheme, consumer loans, the Warm Homes Investment Fund, and other devolved schemes and regulation will all make contributions. However, competing demands for these schemes, such as supporting three million homes to install solar panels, may limit their ability to deliver heat pumps at scale.

2. Getting solar panels on three million homes will stretch the available funding

Solar panels help to reduce bills, and when combined with a heat pump, battery storage and a smart tariff could save a typical household £1,000 per year. However, they have little impact on carbon emissions, and the UK government needs to balance investments in solar against investments to electrify heating.

In the Warm Homes Plan the UK government has set a target of three million homes with solar panels fitted by 2030. We expect up to 800,000 of this target could be fulfilled by the Future Homes Standard, with most new houses having solar fitted, and the remaining 2.2 million through low-income grant schemes or low-cost finance for owner occupiers and landlords. Central to this ambition will be ensuring supply chains have capacity to scale at pace. To hit this target the domestic solar industry needs to grow by 40% per year every year until 2030 - hard, but doable.

Low-cost finance will be key to install solar panels in 2.2 million existing homes

Historically the UK government has not supported many residential solar installations via its schemes. Since 2022 low-income schemes only accounted for 18% of all new rooftop solar installations, although (as with heat pumps) ECO and HUG accounted for a majority of these (57%).

Low-income schemes will get less overall funding in future years than recent ones, but there is scope for them to spend this more effectively than recent schemes, such as ECO4. However, as with heat pumps, the ongoing schemes are not doing a lot of solar, and are unlikely to increase the amount they do in the next year or two. But the future integrated scheme could increase solar installations as part of a wider push to electrify homes and reduce fuel poverty.

Outside of grant-funded schemes, there is potential for new area-based schemes to provide low-income households with solar panels using finance from the Warm Homes Investment Fund. However, as with heat pumps, more work is needed to develop business and delivery models that can translate funding into action.

Most of the remaining 2.2 million installations will need to come from able-to-pay households - both owner occupiers and landlords. Affordable consumer loans could help grow demand for solar from both groups. We do not assume that every homeowner will want to take out a loan to pay for solar panels, but based on demand for solar through the Home Energy Scotland grant and loan scheme, it seems likely to be a popular option.

DESNZ projects that the new minimum energy efficiency standards for the private rented sector could see up to one million homes getting solar panels in order to comply with the regulation. In practice the actual amount will likely be lower as solar will not always be the cheapest route to compliance for many homes. While details of the consumer finance offer need to be fleshed out, we expect it will be a personal loan. This will not suit all landlords, but may be attractive for the 45% of landlords who only own a single property, or the 38% who own between two and four.

The consumer loan scheme has £2 billion to spend, and it seems likely that consumers will be drawing on these loans to support heat pumps and other measures as well as solar panels and batteries. It is hard to estimate how many measures this scheme will support. In practice, we expect the UK government's loan facility will unlock larger pools of private finance that can support more installations, helping to deliver some (or all) of those 2.2 million homes.

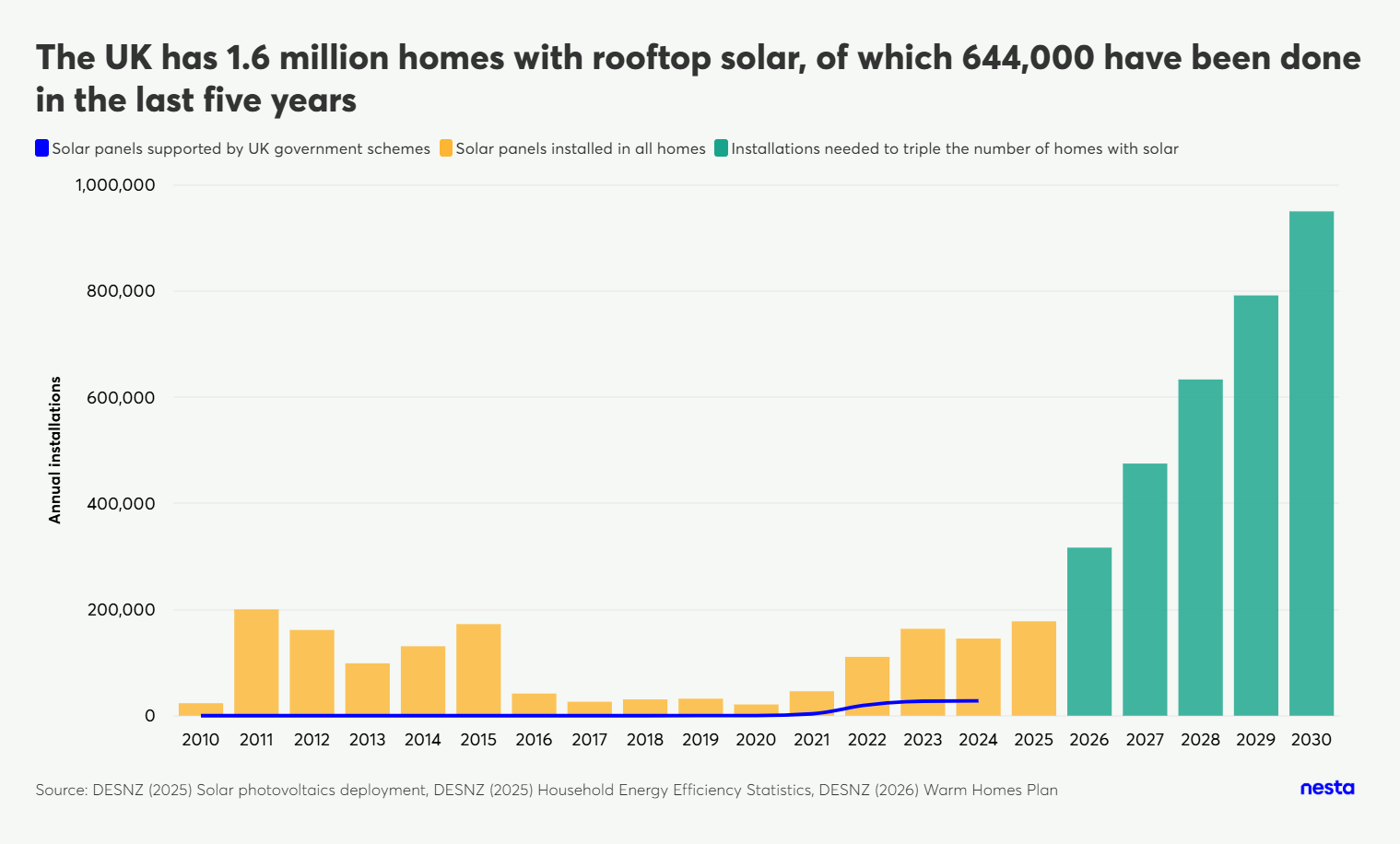

Solar supply chains will need to more than triple their capacity to meet this target

Britain has well established supply chains for solar which have installed panels on over 585,000 homes since 2022. But tripling the number of homes with solar panels will require annual deployment to grow from doing around 175,000 installations today to over 600,000 a year (on average).

The UK has 1.6 million homes with rooftop solar, of which 644,000 have been done in the last five years

Figure 5 - Projected annual residential solar PV installations to 2030

Compared to heat pumps, solar supply chains already have a higher baseline capacity and have demonstrated their ability to scale up rapidly in the past. Annual residential solar installations increased more than fivefold (from 21,200 to almost 110,000) between 2020 and 2022, and then grew by 50% again in 2023. This suggests that it is reasonable to expect solar supply chains to grow faster and further than other technologies in the near future.

That said, hitting the new target will require the UK's domestic solar industry to grow by 40% every year (on average), to do over 950,000 installations in 2030. This target is ambitious but achievable if the UK government provides a consistent, credible and clearly-signalled direction. Long-term commitments on consumer finance, private rented sector standards, grid connections and integrated retrofit programmes will help to unlock investment, expand the workforce and allow supply chains to scale with confidence.

3. Minimum energy efficiency standards are doing most of the heavy lifting to deliver the manifesto target of five million homes improved by 2030

The Warm Homes Plan also aims to deliver the UK government's manifesto commitment to upgrade five million homes to cut bills for families. DESNZ expects that new minimum energy efficiency standards for the private and social rented sectors will improve 2.9 million homes; 58% of all those upgraded under the Warm Homes Plan.

There are over 4.6 million homes in the private rented sector in England, and another 4 million in the social rented sector. They house a disproportionate share of households who are low-income, and a larger share who are fuel poor. Making these homes more efficient will reduce energy bills and lift households out of fuel poverty. Electrification offers the biggest potential efficiency gains, but many of the poorest-performing homes also need better fabric insulation to ensure that their occupants enjoy a decent level of comfort.

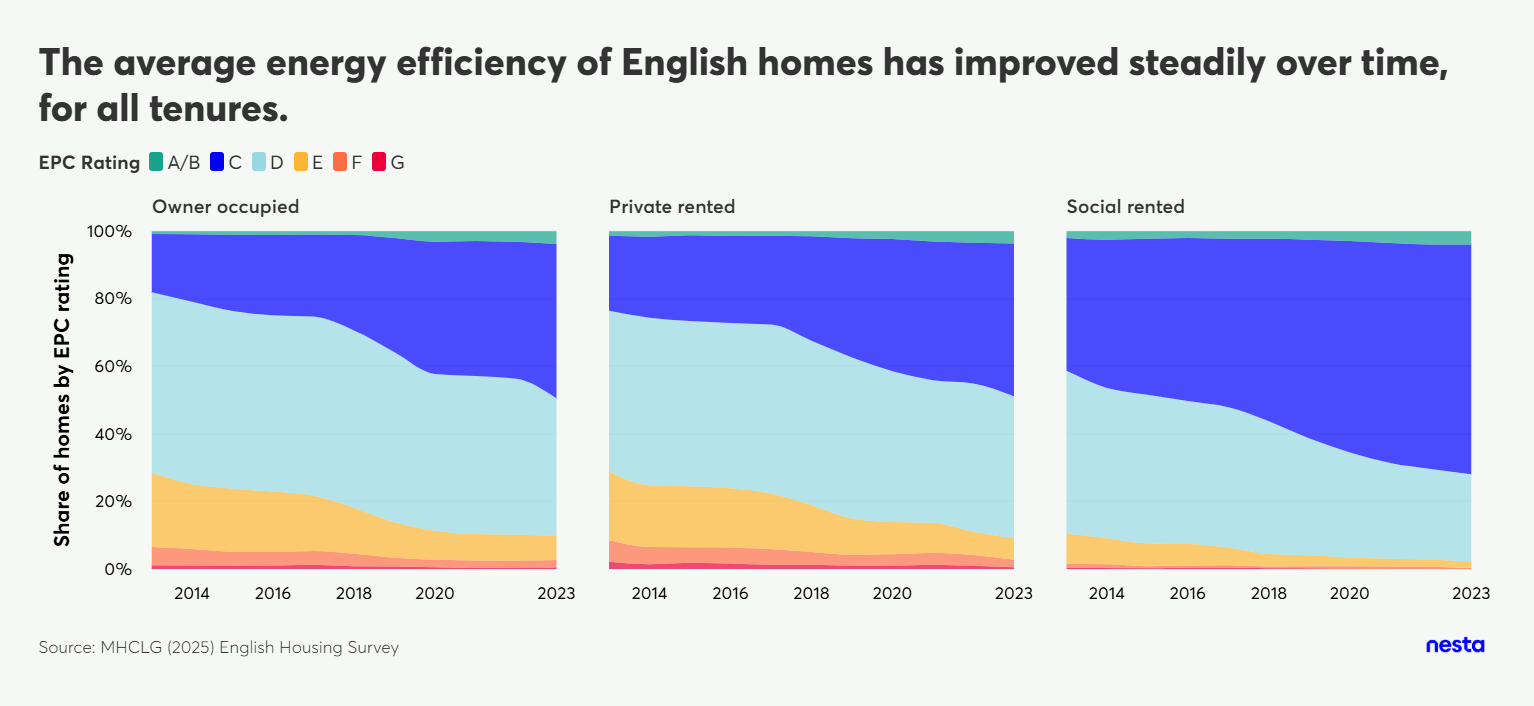

English homes have been getting steadily more efficient over time. Across all tenures, the share rated EPC A-C increased from 23% in 2013 to 53% in 2023. This progress has helped to reduce the total electricity and gas consumption by homes by 17% and 27% (respectively) even as the total number of homes increased by 2.5 million.

The average energy efficiency of English homes has improved steadily over time, for all tenures.

Figure 7 - EPC ratings on housing stock in England

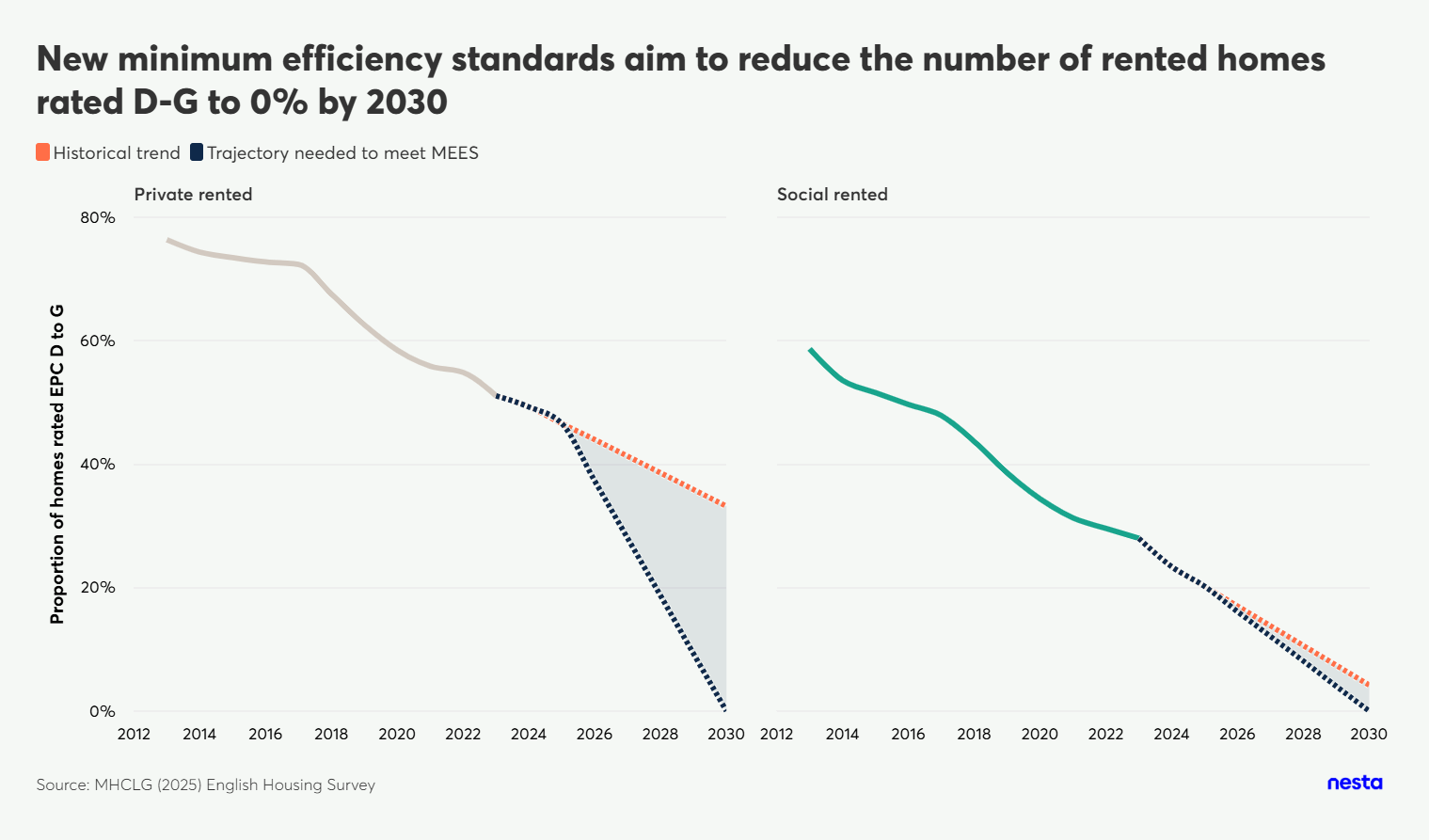

The new standards will require private and social rented homes to reach a minimum standard of EPC C by 2030. DESNZ expects that this will improve 1.7 million private rented homes and 1.3 million social homes.

- The social rented sector is already on track to reach this standard within a few years, with or without regulation. Over 72% of homes in the sector were already at least EPC C in 2024; on its current trajectory this would hit 95% by 2030.

- In contrast, while the private rented sector has improved over time (at roughly the same pace as owner occupied homes), only 49% were EPC C or better in 2024.

The private rented sector needs regulation to accelerate progress on energy efficiency

Private rented homes have been subject to an EPC E minimum standard since 2018, and the proportion failing that standard fell from 9% in 2013 to 3% in 2023. While there is evidence that the regulations drove improvements in the sector, it is difficult to separate this from the overall trends.2 That standard only affected 270,000 homes; the new EPC C minimum will apply to almost 2.8 million. Given its current trajectory, the private rented sector needs regulations to accelerate progress towards higher efficiency standards by 2030.

New minimum efficiency standards aim to reduce the number of rented homes rated D-G to 0% by 2030

Figure 8 - Projected proportion of homes with low energy efficiency ratings based on historic trends vs. the trajectory required to meet 2030 energy efficiency targets

- The main aim of these standards is to improve the welfare of poorer households, rather than meet climate targets. Once implemented, DESNZ expects that they will only account for 3% of the abatement from buildings in the fifth carbon budget.

- The private rented sector has the highest proportion of households in fuel poverty - 22% compared to 8% for owner occupiers or 13% for social housing. Under the UK government's measure of fuel poverty, there were 933,000 fuel poor households living in private rented homes in 2024.

- Under the UK government's definition of fuel poverty (the Low Income, Low Energy Efficiency metric, or LILEE), any household living in a home rated EPC C or better is automatically no longer fuel poor. So if the minimum standard is implemented in all rented homes, fuel poverty will fall by 933,000.

This is the single most significant policy in the Warm Homes Plan in terms of the volume of homes affected and its potential to reduce fuel poverty. In addition to the targets discussed above, the Warm Homes Plan includes a goal of taking 1 million households out of fuel poverty by 2030. It will be hard to make substantive progress against this target if DESNZ cannot - through carrots or sticks - drive progress towards this standard. While the low-income grant schemes offer a better guarantee of targeted help for fuel poor households, the volume of homes that will be upgraded is far smaller.

The design of the minimum standard regulations will affect the type of measures installed

DESNZ reduced the cost cap for landlords from £15,000 to £10,000 following consultation (this sets a limit on how much they are required to spend to meet the standard). And the actual standard that needs to be met will change as the EPC system undergoes long-overdue reforms in the near future. Reducing the cost cap does not necessarily reduce the number of homes that get upgraded; but it will affect the types of measures that get installed.

- Under a £10,000 cost cap the number of private rented homes getting solid wall insulation falls by 92% (relative to the higher cap).3 This change also reduces the upper bound number of homes getting solar panels by 170,000, (an 8% decrease).

- While these regulations could drive heat pump uptake, DESNZ's preferred option does not actively incentivise them over other measures. The general approach will

focus on making homes heat pump ready with fabric upgrades and smart technologies.

The Seventh Carbon Budget implies that around 149,000 private rented homes will get heat pumps between 2026 and 2030 (14% of all domestic retrofit heat pumps in that period). It may be that pushing the private rented sector to be fully ready for heat pumps (and other types of low-carbon heating) by 2030 will make it cheaper and easier to make faster progress in subsequent years. But any near-term shortfall will make it harder to meet interim climate targets, such as the 2030 NDC and Fifth Carbon Budget.

Moving from targets to delivery

The UK government has made a credible case that the Warm Homes Plan can deliver on its ambitions. Its success or failure will rest on DESNZ's ability to execute the plan across finely balanced delivery pathways: sustained growth in the Boiler Upgrade Scheme alongside the new finance and low-income models for heat pumps, affordable customer finance and rapid supply chain scaling for solar, and the effective implementation of minimum energy efficiency standards.

Even with its funding settlement, the Warm Homes Plan has created competing demands in delivery, particularly between heat pumps and solar, that may end up competing for the resources of schemes such as the Warm Homes Investment Fund. There are also risks beyond DESNZ's control, such as energy prices and the capacity of local authorities, but the plan shows a clear awareness of these challenges.

While margins for error remain slim, sustained policy clarity and a strong focus on delivery mean the Warm Homes Plan has laid strong foundations to meet its targets.

-

DESNZ (2026) Warm Homes Plan: Technical annex ↩

-

Resolution Foundation (2022) Hitting a brick wall ↩

-

DESNZ (2025) Improving the energy performance of privately rented homes: options assessment (OA) ↩