Economics explained: why most policies to deal with the energy price shock are inefficient

www.nesta.org.uk/blog/economics-explained-why-most-policies-to-deal-with-the-energy-price-shock-are-inefficient/

www.nesta.org.uk/blog/economics-explained-why-most-policies-to-deal-with-the-energy-price-shock-are-inefficient/

www.nesta.org.uk/blog/economics-explained-why-most-policies-to-deal-with-the-energy-price-shock-are-inefficient/

www.nesta.org.uk/blog/economics-explained-why-most-policies-to-deal-with-the-energy-price-shock-are-inefficient/

The conflict in Iran has led to a rise in oil and gas prices, with knock-on effects on the wider economy. As a net importer of these commodities, the UK is particularly affected by this shock - with fuel prices rising by 20% to 30% and wholesale gas and electricity prices going up.

As with all crises, many policy solutions have been proposed, such as VAT cuts and cash transfers to consumers with no strings attached. These proposals focus on relieving some of the pressure on consumers and are described as untargeted measures because they apply to everyone.

Unfortunately, while these policies are well intended, they could do more harm than good.

In this explainer I walk through the economic theory behind impacts of oil price shocks on the economy, as well as the concepts behind responsive policy proposals and their impacts.

An oil price shock, often referred to as negative supply shock, is when the supply of oil goes down in response to an unexpected event, such as war, pandemics, or extreme weather events. As a result, there will be a relative price increase of oil compared to the prices of other goods. This is not yet called inflation, as inflation refers to a general price rise of multiple goods, as we’ll explain below.

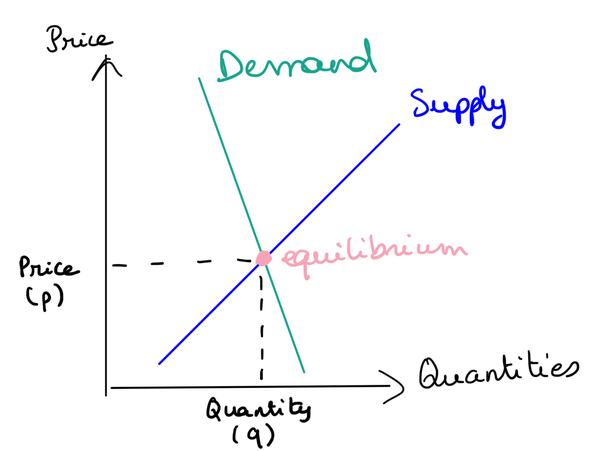

Let’s consider the market for oil production. Figure 1 below plots the quantities of oil that consumers demand (green demand curve) and the quantities supplied (blue supply curve) at each given price. Standard demand curves are downward sloping: the more the price rises, the fewer quantities people will want. In oil markets, the demand curve is particularly steep, reflecting that consumers are not able to easily reduce their oil use when the price rises, meaning their demand is relatively inelastic. The supply curve is upward sloping to reflect that the higher the price, the more producers will be willing to supply the market.

The equilibrium is found where supply meets demand, that is when these two curves intersect, setting the quantity and price of oil supplied to the market.

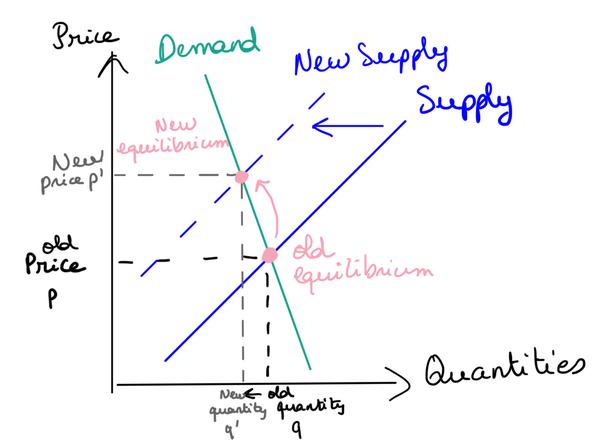

Consider a negative supply shock to the oil market. If oil suppliers’ production costs suddenly increase - because ships are being delayed for example - they raise their prices as a result. Mechanically, the quantity supplied goes down and the price is higher. The higher price reflects the unavoidable new reality that resources are scarcer.

This choice is shown in Figure 2, where the new supply curve has moved to the left. Without intervention, the new equilibrium is when the new supply curve (in dotted blue) meets the original demand curve (green).

Figure 2 : Effect of oil price shock on the equilibrium

As a result, society now needs to make a choice: decide who reduces their consumption of oil or accept a higher price. Some people will be able to adapt, by choosing the train over a flight, exchanging an oil boiler for a heat pump, or consuming less energy. By reflecting the 'market truth’, high prices push the economy toward efficiency. But there is a catch: market efficiency doesn’t distinguish between what is a luxury choice and an essential need.

The least desirable outcome is that the person who can no longer afford the new price is the one that needs the energy most. It therefore raises a question for governments about whether, where and how to intervene to shape the market.

The policy responses that are usually put forward in response to a negative supply shock revolve around three pillars.

How do these policies play out in our example? Let’s go back to our diagram.

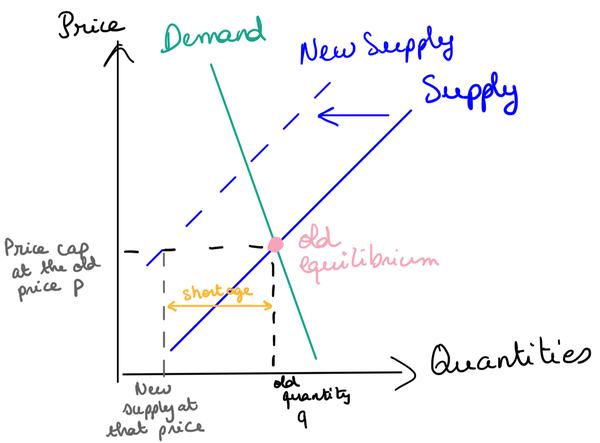

Price cap below cost: A price cap requires firms to fund the difference between the new higher price and the capped price themselves. In this situation, demand is unchanged (the price has not moved), but suppliers face higher costs which they cannot pass on given the price cap. Some will be able to meet the price cap - by tapping into their margins or their reserves - but some will not be able to sell at the capped price, as they would make a loss. They thus decline to supply the extra litres of oil, causing a shortage, in the yellow curve below.

Figure 3: Effect of a price cap below cost on the economy

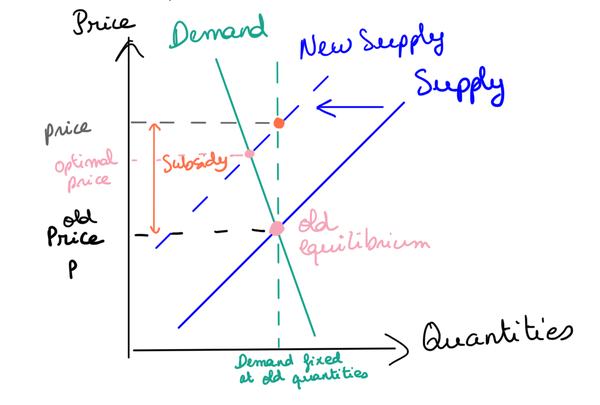

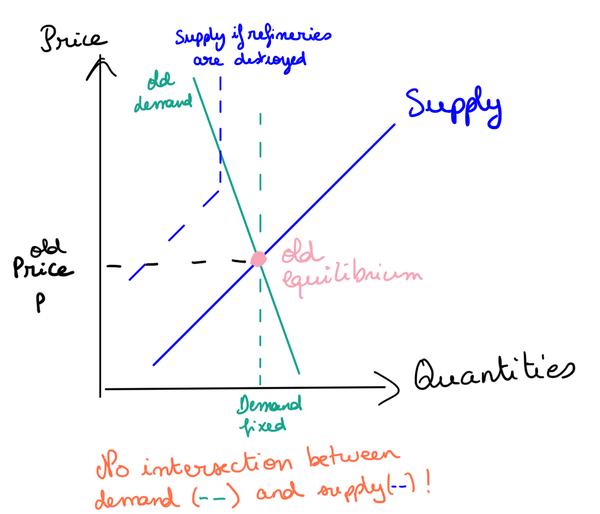

Subsidies: If the government instead pays the difference between the previous lower price and the new higher price, this artificially reduces the price signal. This means consumers will continue asking for the same quantity as before, without thinking of the price. For example, this happens in student accommodation where bills are included in a fixed fee: residents don’t pay attention to prices and consume irrespective of the real cost of energy. Shown in Figure 4, In our diagram, the demand is fixed at the old quantities. No one makes an effort to adjust to the new reality.

In a world where supply has become more expensive but could still satisfy the whole market, this would only be fiscally inefficient. But if there is a real, physical, constraint that a maximum quantity of oil that can be supplied - perhaps because oil ships cannot deliver to the UK - the supply curve becomes vertical after that point. This means people can pay any price but the quantity supplied is stuck. There is nowhere where supply meets demand, meaning the price will go up and up (technically until infinity), with the bill paid by government payouts, which is another word for taxpayers’ money.

Figure 5: Unravelling of the equilibrium if there is a real supply constraint

Untargeted cash transfers: Cash transfers – where the government sends consumers money to compensate increased prices – are usually unconditional.

The impact of this is that, rather than using less oil due to an increased price, consumers utilise this increase in income by consuming more of the other goods altogether. Overall demand goes up in the economy, and this brings inflation.

Countries that have implemented the above policies in response to negative supply shocks in the past - for example in the Covid 19 pandemic, or when responding to Russia’s invasion of Ukraine - often ended up with high inflation. Here’s why.

Untargeted cash transfers are widely criticised for driving inflation. To understand why, imagine an economy where revenue is split between oil and other goods.

When the oil price doubles, consumers naturally cut back on fuel. If the government sends everyone money to offset those energy costs, people will inevitably spend that extra cash on non-oil goods. However, the supply of other goods has not changed - if anything it has shrunk because businesses find it harder to produce. This means that the economy overheats, because more demand fights for the same supply or, as economists say, “too much money chases too few goods”. This is inflation.

Policies that require government spending (for example, funding a subsidy, a VAT exemption, untargeted cash transfers) carry a heavy inflationary risk. In fact, we have seen inflation go up in many countries that implemented these policies after several similar supply shocks.

This is because when a government borrows normally, investors assume the debt will be repaid through future surpluses generated by future growth and tax revenue. In normal times, the central bank can raise the interest rates to fight inflation without worrying about the knock on effects on the government’s debt.

However, when a government’s debt becomes unsustainable, the central bank – the Bank of England in the UK – faces a fiscal dominance trap. Under fiscal dominance, the central bank is reluctant to curb inflation by raising interest rates, because it realises this will increase government interest rate payments on debt. This means they let inflation rise. Once investors and citizens anticipate that inflation is happening, a vicious cycle begins. For example, investors ask for a higher return to counteract inflationary impacts, or citizens ask for higher wages - both resulting in further inflation, causing a hyper inflation loop and leading to a self-fulfilling prophecy.

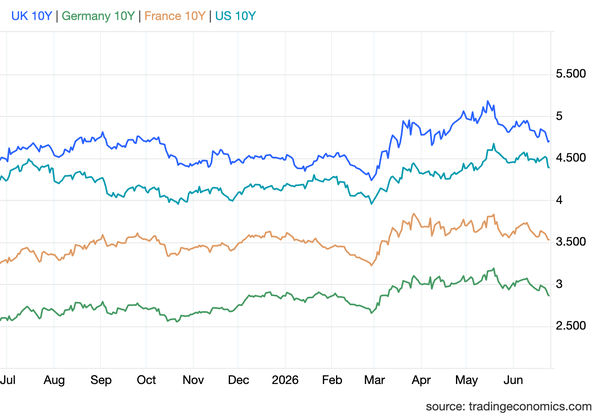

The UK is in a particularly risky position to embark on excessive borrowing as it already has one of the highest borrowing rates among many advanced economies (see Figure 5). This means that any excessive borrowing could lead to a spike in the rate of return investors require. On top of causing higher interest rates payments, the extreme case would be if the UK debt became unsustainable, with potential risks of defaults. In particular, as the announcements on policies to face the energy crisis were made, markets immediately reacted negatively, with the rate on government debt spiking in the UK.

Figure 5: Comparison of the 10-year borrowing rates between FR, UK, DE and US (%) Source: Trading Economics

Recognising this risk, some policies propose to fund the cost of these policies with general taxation. This may be deflationary, because we reduce the disposable income of agents in the economy, and they will thus consume less of all goods in general. This could partially alleviate the inflationary pressure, but this is still inefficient, since the policy is regressive - as I argue below.

Some argue that policies such as price caps reduce inflation. However, though they may in theory mechanically reduce inflation metrics, this tends to be true only in the short run. In the long run, these policies result in hidden inflationary costs.

This is because the price cap leads to shortages of these goods, which have a hidden monetary cost. For example, petrol station closures mean consumers now have to drive further in search for an open one. And more queues at the remaining pumps that are open mean that people spend more time and resources. This time is money, and it is costly (what economists refer to as the “opportunity cost”: in that time waiting, consumers could have worked and earned a salary).

On top of removing the price signal – and therefore preventing consumer behaviour from changing - price caps and subsidies often benefit the richest households. Richer households tend to consume more products, and oil in particular. This means they will effectively receive more of the subsidy money, making it an inefficient policy.

Lastly, in a world where there is actual, world-wide rationing, a blanket subsidy may fuel the fire. The UK would, in this case, compete for the same oil as before with other countries, leading to an even greater price increase in the world markets. This means that more money would be inefficiently spent, in addition to causing shortages in other countries that cannot afford to outbid us. This is what we see in South East Asian countries, which are required to implement actual rationing policies because they cannot face the costs of higher energy prices. This may also have ripple effects on domestic inflation, as we import from these countries.

These untargeted measures carry unintended consequences that can negatively impact the economy in the long term, leaving countries more economically vulnerable when future shocks arise. Here are three things they could do instead.

Support consumers to reduce oil demand

The fact is that the crisis has revealed that the world has changed and is now constrained. There are fewer resources we can use. This is a physical reality that cannot be overridden by economic measures. Some consumers will have to reduce their consumption. This is not necessarily bad: the oil price shock can be the trigger to new investments in energy efficiency measures that are now commercially viable, as the net present value of these new projects becomes positive. Instead of trying to override this effect, governments could support this transition by encouraging energy efficiency measures – such as reducing demand during peak hours – or moving to heating technologies that do not rely on gas, such as heat pumps.

Introduce targeted cash transfers

But what we saw during the energy crisis, which we cannot ignore, is that it led some people to make difficult decisions in light of the cost of living crisis; having to choose between heating and cooking, for example. This is why most economists suggest implementing targeted cash transfers. The idea is to transfer money to the people that need it - the poorest - where need is determined by a certain income threshold combined with energy expenditures.

Why does this work? By not changing the prices in the oil market, every consumer will feel the increase and will try to reduce their consumption where possible. But the poorest will no longer have to reduce the consumption of other goods. This would not be as inflationary as the untargeted measures because it would only be a share of the population that would benefit from the measure. This can be funded by the extra VAT revenues that the government makes, making it revenue neutral.

In practice, targeting the poorest is difficult. As our Chief Economist Tim Leunig argues, restricting support to people receiving benefits from the government is not necessarily the best identifier of citizens in fuel poverty. To refine these measures, the UK government could leverage the extensive data from satellites and buildings (for example Energy Performance Certificates, gridded temperature) to better identify recipients in need.

Rebalance costs from electricity to gas

The best way to tackle economic shocks from fossil fuels is to stop using them altogether. But to do this, Britain needs to lower the cost of its electricity, to make heat pumps and EVs more attractive than their fossil fuel equivalent. Many proposals, and Nesta’s in particular, suggest using the current crisis to do that, by rebalancing the prices between electricity and gas. The UK has one of the highest electricity to gas price ratios, which discourages people to switch to electricity and reduce their reliance on gas. We are suffering from these policy choices. The rationale behind lowering the electricity price, by removing the policy costs for example, is not only motivated by the current energy crisis, but also by the fact that electricity is increasingly coming from cleaner homegrown sources while gas is more polluting. Our proposals suggest removing these distortions in order to encourage more people to switch to electricity.

Fossil fuel shocks are extremely painful, and blanket government interventions can usually only defer the pain. The best responses are well targeted at those most in need, they encourage using energy more efficiently and ultimately encourage people to stop using fossil fuels altogether. That is the only reliable remedy to the pain.