Nesta has been researching the ways to roll out area-based approaches to clean heat at scale

One aspect of our clean heat neighbourhood approach is shared infrastructure technologies, such as networked heat pumps, shared ground loops, and communal and district heat networks. These will be the most appropriate clean heat solution for many city centres and densely populated areas. If used appropriately, these technologies are highly efficient, can make use of local resources such as waste heat, and create opportunities for long-term stable income thanks to their long lifespan.

In practice, though, these shared infrastructure projects often encounter financial and commercial difficulties that can slow down their delivery and prevent them from scaling.

We interviewed project leads, policymakers, institutional finance actors and industry experts to understand the reasons behind the challenges faced by shared infrastructure projects across the UK.

What’s in the report

- Shared infrastructure projects require a large financial outlay and have a long payback period.

- They can be delivered through various arrangements, either directly by a local authority, a private company or through a partnership between the public and private sector which can spread the risks between partners.

- While individual projects have been developed across the UK, they have often struggled to achieve scale, leading to a larger pipeline issue, which has meant that larger financial actors have not entered the market at the pace required to reach decarbonisation targets.

- Structural challenges, such as the high cost of electricity relative to gas, currently weaken the business case for shared infrastructure.

- The research in this report suggests that the coordination failures between local authorities, developers and investors in the UK’s shared clean heat infrastructure sectors should be addressed by UK and devolved government action.

Recommendations

The following is required to scale up the delivery of shared infrastructure projects.

- The UK and devolved governments should address the low certainty of demand and improve the economics of individual projects by:

- using mandates to connect, and building regulations to guarantee uptake from a range of offtakers, and lower risk for developers

- encouraging lowering the cost of heat at the source through supporting local authorities in mapping sources of waste heat, encouraging connections with local sources of energy generation or waste heat, and mandating connections to clean heat projects to guarantee a stronger business case

- giving local authorities responsibility for pooling investment by giving them additional capacity through revenue funding, in order to create a stronger project pipeline.

- In addition, the UK government should increase the amount of capital available for clean heat projects through:

- a strategic investment fund to support projects across tenure and technologies

- taking an equity stake in clean heat projects in order to de-risk them, attract other forms of private investment (such as debt finance) and create more opportunities for long-term sustainable assets to generate returns on investment, using the financial transactions included in the Warm Homes Plan.

Authors Marine Furet, Josh Jackson and Robin Parker

- Glossary

- Executive summary

- Introduction

- Economic characteristics of shared infrastructure

- The current subsidy landscape

- What are the current economic blockers to area-based clean heat schemes?

- Lessons from different approaches to infrastructure funding

- Policy opportunities for area-based approaches to clean heat

- Conclusions: Proposed policy approaches and solutions for scaling clean heat neighbourhoods

Glossary

Energy and infrastructure

Heat networks

A heat network distributes heat across a building (communal heat network) or a range of buildings (district heat network) via a set of pipes. The heat can come from a centralised heat pump or energy centre, and be derived from a variety of sources (water, ground or energy from waste). At user level, heat is distributed via an individual heat interface unit.

| Generation | Source of heat | Needs an energy centre? | High or low temp. | Network | Use cases |

|---|---|---|---|---|---|

| Third | Centralised (gas boiler or heat pump) | Yes | High (90-70°C) | Insulated pipes | Densely built environments (e.g. city centre, new-build development) |

| Fourth | Centralised, either from heat pump or energy from waste | Yes | High (70°C) | Insulated pipes | Densely built environments (e.g. city centre, new-build development) |

| Fifth | Decentralised, from a network of heat pumps in each building (in some instances, a centralised heat pump maintains temperature across all units) | No | Low (10-30°C) | Pipes can be less insulated | Mixed, including industrial |

Energy centre

The name given to a building that hosts the heat pump, cooling and/or energy generation element of a heat network.

Offtaker

The buyer of the heat produced by a heat network, who may be its direct consumer or purchase it for resale.

RIIO

RIIO stands for ‘Revenue = Incentives + Innovation + Outputs’ and is the energy price control framework used by Ofgem. ED stands for Energy Distribution. The RIIO-ED2 framework applies to electricity distribution networks for the period going from 2023 to 2028. ED3 is Ofgem's next electricity price control framework, which will start in 2028 and run until 2033.

Shared (or ambient) ground loop

A system where multiple properties are connected to a communal ground loop array and boreholes. A shared ground loop is a category of fifth-generation heat network and is treated as a heat network in regulatory terms.

Finance terms

Blended finance

A type of structured finance intended to accommodate different risk profiles and rates of return, generally through combining a public or philanthropic investor, which will assume the greater risks linked with the project or portfolio, and private capital.

Debt-based financing

A process for a business to raise funds by borrowing capital, which must be repaid over time, such as by taking out a loan or through selling bonds. Unlike equity, where investors become co-owners of a company, debt financing preserves a company's ownership structure.

Equity-based financing

In equity-based financing, a business can raise capital by selling shares to investors. Equity investors make a return on their investment either by selling their shares or receiving dividends.

First-loss capital / Junior / Senior tranche

In blended finance, the junior tranche of a fund will be first to assume any potential losses from a project (first-loss capital) while the more senior tranche of a fund will be the first to receive any proceeds or interests and recover its initial investment. The first-loss or junior tranche is therefore more exposed to any risks, such as defaults on repayments. This priority-based structure of repayment is called a waterfall structure.

Patient capital

Patient capital is a long-term investment, which can include either debt or equity finance.

Executive summary

With a cumulated investment estimated at £209 billion for the UK, the clean heat transition represents a colossal opportunity to unlock public and private investments. This includes communal and district heating technologies such as heat networks and shared ground loops, which are estimated to represent a £60-80 billion investment. Investing in shared infrastructure has the potential to support local job creation and improve the efficiency of home heating systems across the UK, while tapping into existing local energy sources, such as renewable generation sites and waste heat.

At present, however, a series of structural blockers have hampered the economics of individual clean heat projects and prevented delivery at scale. This report investigates which economic barriers stand in the way of building shared heating infrastructure. It proposes solutions that can allow more projects to be commercially successful, overcome structural barriers and support delivery to scale nationally.

Key findings

- There are a range of ways to finance and deliver shared infrastructure for clean heat, from fully publicly owned heat networks to public-private partnerships and fully private developments.

- The financial viability of individual projects is primarily determined by their capacity to secure sufficient customer uptake to offset initial capital expenditure. To be attractive to investors, projects must demonstrate, with a high degree of certainty, that they can secure stable demand from a range of offtakers (or buyers of the heat produced by the heat network). A lack of regulatory incentives makes this challenging for domestic retrofitting in particular, with investors prioritising new-build projects.

- Challenges in securing funding for individual projects have prevented a national pipeline of investable projects from developing. This has in turn prevented large institutional financial actors from entering the sector and further limited the investment pool for projects. This vicious cycle was identified by stakeholders as the 'pipeline problem'.

- The high cost of electricity relative to gas generates a higher cost of heat for low-carbon projects, creating unfavourable business cases when compared to legacy systems such as those reliant on gas boilers.

- Low capacity at local authority level has limited their ability to conduct delivery-oriented clean heat planning, resulting in sporadic and limited approaches to clean heat projects.

Policy solutions for viable projects

- The research in this report suggests that the coordination failures between local authorities, developers and investors in the UK's shared clean heat infrastructure sectors would be best addressed by government action.

- The UK and devolved governments should address low certainty of demand and improve the economics of individual projects by:

- Using mandates to connect, and building regulations to guarantee uptake from, a range of offtakers, and lower risk for developers

- Encouraging lowering the cost of heat at the source through supporting local authorities in mapping sources of waste heat, encouraging connections with local sources of energy generation or waste heat, and mandating connections to clean heat projects to guarantee a stronger business case

- Giving local authorities responsibility for pooling investment by giving them additional capacity through revenue funding, in order to create a stronger project pipeline.

- In addition, the UK government should increase the amount of capital available for clean heat projects through:

- A strategic investment fund to support projects across tenure and technologies

- Taking an equity stake in clean heat projects in order to de-risk them, attract other forms of private investment (such as debt finance) and create more opportunities for long-term sustainable assets to generate returns on investment, using the financial transactions included in the Warm Homes Plan.

Introduction

Nesta has been advocating for a technology agnostic, area-based approach to clean heat planning and delivery that would cover all tenures and technologies. We believe that communities should be empowered to access the clean heating solutions that are the most efficient and best fit for their particular location and needs. Those solutions will vary for different homes and neighbourhoods, with individual heat sources (such as air source heat pumps) right for some homes, and shared systems (such as heat networks or networked heat pumps) right for others. Despite some promising pockets of innovation, across the UK area-based approaches to clean heat currently struggle to scale at the pace required to meet the ambition of decarbonising our housing stock by 2050.

Area-based approaches to clean heat have the potential to offer a more cost-effective approach to decarbonisation. They can make economies of scale possible, for example by enabling group purchases or by lowering the costs of installation through coordinating the work. They can also allow for more efficient technologies, such as ground arrays, which can both reduce the strain on the grid and reduce long-term costs to consumers. Finally, in some areas, they can also unlock the use of shared infrastructure technologies, such as shared ground loops and heat networks, that are not accessible to individual consumers. These technologies are not appropriate to every location, but can open up access to longer term or more patient finance.

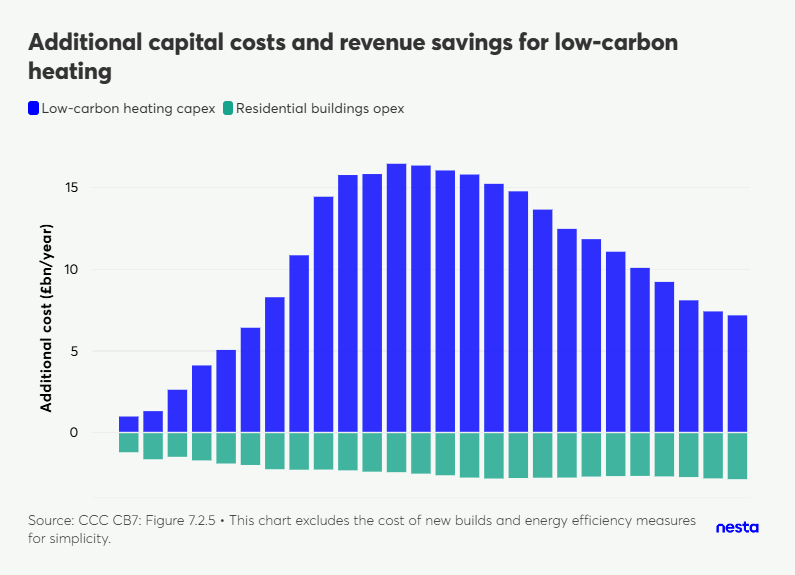

But clean heat will demand large-scale investment. The Seventh Carbon Budget (CB7) estimates the necessary investment in low-carbon heating between today and 2050 at £209 billion (see Figure 1) for the whole of the UK. While the Climate Change Committee's (CCC) Balanced Net Zero Pathway predicts a gradual decrease in the unit and operating costs of technologies (CCC CB7, Figure 1) between 2026 and 2050, this sum cannot be absorbed by subsidies and grants alone, and will require a blend of public and private capital. This is a significant opportunity for clean heat neighbourhoods, particularly for projects centered on shared-infrastructure projects such as heat networks and shared ground loops, which have the potential to attract finance.

Figure 1. Additional capital costs and revenue savings for low-carbon heating

Figure 1. Additional capital costs and revenue savings for low-carbon heating

The turn to area-based delivery of clean heat

In the last few years, both the UK and devolved governments have been wrestling with the problem of scaling clean heat delivery, in a challenging context dominated by increasing constraints on public spending, the high cost of electricity, and a sharp rise in poverty across the country. While many local and combined authorities have formulated decarbonisation plans (and in some cases pioneered area-based approaches to deliver them), a large number of areas still struggle to leverage the required funding and local resources to bring projects to delivery. With this project, we investigated some of the reasons behind this issue, and here present some potential solutions and models available to the UK government, devolved governments and local authorities.

Recent developments in policy are transforming the context for clean heat delivery at scale. The recently published Warm Homes Plan calls for a strategic, place-based approach to clean heat overseen by a new Warm Homes Agency, created to both support delivery and stimulate investment. The Warm Homes Plan also champions the role of local governments, but provides fewer details as to the intended governance of area-based clean heat, merely suggesting an enhanced role for Distribution Network Operators (DNOs) alongside different levels of local government. Furthermore, the remit of the Warm Homes Agency in Wales and Scotland will need further clarification and, with upcoming devolved elections in May 2026, there is an opportunity for the devolved nations to devise a way forward based on learnings from the Advanced Heat Zoning programme and Warm Homes Plan Barnett consequentials.

At the regional level, the turn to area-based coordination is also supported by the creation of new bodies: the Regional Strategic Energy Planners (RESP), whose role is to support and maximise investment across the grid, working in partnership with local stakeholders including local government and DNOs to understand local demand and anticipate the investment need, feeding in turn into the National System Energy Operator's RIIO-ED2 and forthcoming ED3 process.

Research questions and key findings

In this paper, we explore the problems faced by coordinated approaches to clean heat projects, to understand:

- Whether they are caused by structural approaches to funding, finance or both

- Whether they are specific to technologies or tenure types

- Whether it is possible to identify solutions to those challenges, and to define some criteria for projects to be successful.

In our research, we have focused mostly on shared infrastructure projects, which face particular economic challenges and opportunities. While there is no one silver bullet to the challenge of clean heat, this paper argues for a two-pronged approach to help projects reach the scale required.

We make the case that the UK government should reduce the uncertainty of demand for clean heat through creating a regulatory framework more favourable to clean heat, helping secure greater uptake and building a pipeline of projects to attract investors. It should also increase the amount of capital available to projects, including through taking equity stakes in clean heat projects to create secure long-term assets.

Economic characteristics of shared infrastructure

Summary

- While individual solutions such as air source heat pumps will suit many homes across the UK in the clean heat transition, in some locations shared technologies, such as networked heat pumps and district heat networks, can be a more cost-effective means of decarbonising homes.

- Shared technologies can also enable location-based synergies, such as industrial heat recovery and co-location with renewable energy generation.

- Understanding the different benefits and risks associated with various ownership models is an important step in the journey towards home decarbonisation, if local authorities are to become a key partner.

Heat networks currently meet an estimated 2% of the UK's domestic heat demand. Of the 11,847 registered heat networks established in the UK, 90% use gas as their main source of fuel and only 3% use heat pumps, and the majority of British households continue to be heated by gas boilers. The UK government's headline ambition is for 20% of UK heat demand to be met by heat networks by 2050, representing an investment opportunity estimated at £80 billion.

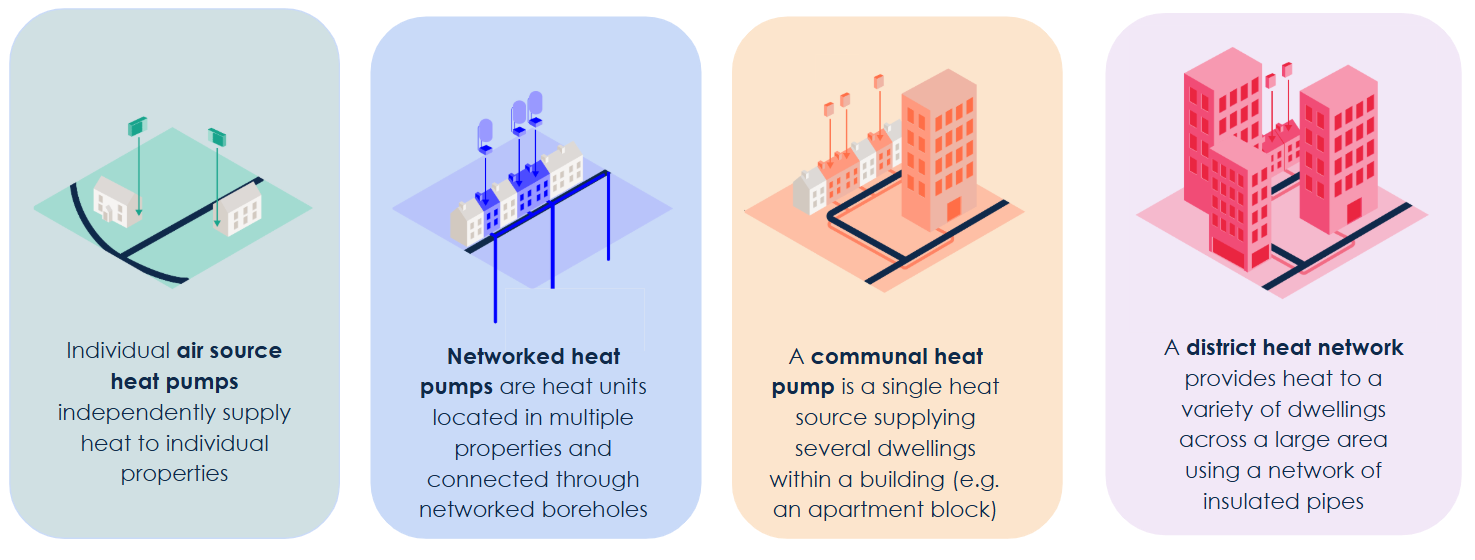

Features of individual and shared clean heat technologies

Figure 2. Clean heat technologies

Figure 2. Clean heat technologies

Individual technologies

Individual air or ground source heat pumps deliver heat straight to a consumer, but they still need to pay a supplier for the energy the unit itself runs on. In most cases the homeowner will own their heating hardware themselves, but some will lease it. All of these heating systems will be directly located in people's properties. Their cost varies depending on size, ranging from £10,000 to £16,000 for an individual air source heat pump (ASHP) or £20,000 to £37,000 for a ground source heat pump (GSHP).1 If installed in greater numbers, however, they can also result in additional costs to strengthen energy infrastructure and avoid grid congestion. Areas with limited grid headroom and where an alternative source of heat is present may therefore present opportunities for the development of shared infrastructure.

Shared infrastructure

Shared infrastructure ranges in scale, from a communal heat pump that covers multiple dwellings within a single building to systems capable of supplying heat to a whole area (e.g. a city centre), known as a 'district heat network'. The cost and ownership structure of shared infrastructure may be divided between operator and consumer, or rest wholly with the supplier or operator of the clean heat technology. Ownership of and responsibility for maintaining the heat interface units (HIU) that supply heat to residents in a heat network or communal heat pump system may lie with the homeowner or leaseholder of the building, or with the landlord (in the case of a social housing development). Assets such as the energy centre, communal heat pump and pipes are typically owned by the heat network operator. Some infrastructure projects, such as networked ground source heat pumps (which do not include an energy centre), may also be owned through a split-ownership model – this means that the heat pump itself will be the property of the homeowner while the networks of pipes and boreholes will belong to the developer. These features make heat networks and shared ground loops more comparable to infrastructure technologies.

Shared infrastructures such as ambient ground loops and heat networks can serve a range of users or 'offtakers'. These can be residential, industrial or public users. Shared infrastructure technologies can recover their costs through a variable heat charge and fixed connection fees, and standing charges for use and maintenance, paid over the lifetime of the asset. As of January 2026, Ofgem is the designated regulated body for heat networks in the UK, and heat networks and shared ground loops are compelled to provide consumers with a transparent billing breakdown that is based on actual usage.

Given their characteristics, heat networks are particularly well suited to single-ownership projects, such as new-build developments, housing associations projects, or blocks of flats, where less coordination is required between individual homeowners.

Shared-infrastructure technologies typically have higher upfront costs and longer capital recovery periods, which can make them challenging to adapt to the domestic retrofit market. Costs of shared-infrastructure projects are highly project-specific and vary based on factors such as the size and presence of an energy centre, length of piping network and presence of a heat source.

A comparative analysis of a fourth and fifth generation heat network, for example, found that the distribution network of a heat network could make up to 40–45% of capital costs, with the energy centre account for 25–30%.

Heat networks create opportunities to tap into waste or excess heat generated from commercial or industrial sources (currently, over 50% of the heat created through industrial processes is estimated to be wasted). Waste heat can be categorised into high (over 400°C), medium (100 to 400°C) or low-grade heat (100°C or below). The latter is well adapted to recovery for domestic heat, with the potential to use a heat pump to adjust the temperature if required. Several processes can lead to waste or excess heat, including those in industry, as well as power generation, waste incineration and the treatment of waste water. Some locations may also benefit from favourable conditions for ambient heat recovery from the ground, water or air.

Opportunities for waste heat recovery include infrastructures such as data centres, which are currently being developed across the UK, including through the UK government's AI growth zones, with research suggesting this waste heat could heat up to 6.3 million households. There is early evidence that a majority of the British public (56%) would support new data centres being built in their local area, a positive finding driven in the main by the hope for local job creation and lower energy bills. This could support an argument for developers to explore building heat networks alongside a data centre or another piece of public infrastructure generating waste heat, as a way of producing greater co-benefits for communities. Co-locating heat networks with sources of waste heat and/or electricity generation creates an opportunity to reduce the cost of heating for consumers and cooling, which may go some way towards alleviating the impact of the gas-to-electricity cost ratio. Projects can also offset the potentially higher cost of heat through combining shared-heating infrastructure with other benefits.

For example, some projects have found success through co-locating with renewable energy generation to reduce the cost of heat in the network, such as the proposed Morecambe Bay Community Renewables heat network, which aims to use locally generated renewable energy from a wind turbine to reduce the cost of heating from the heat network.

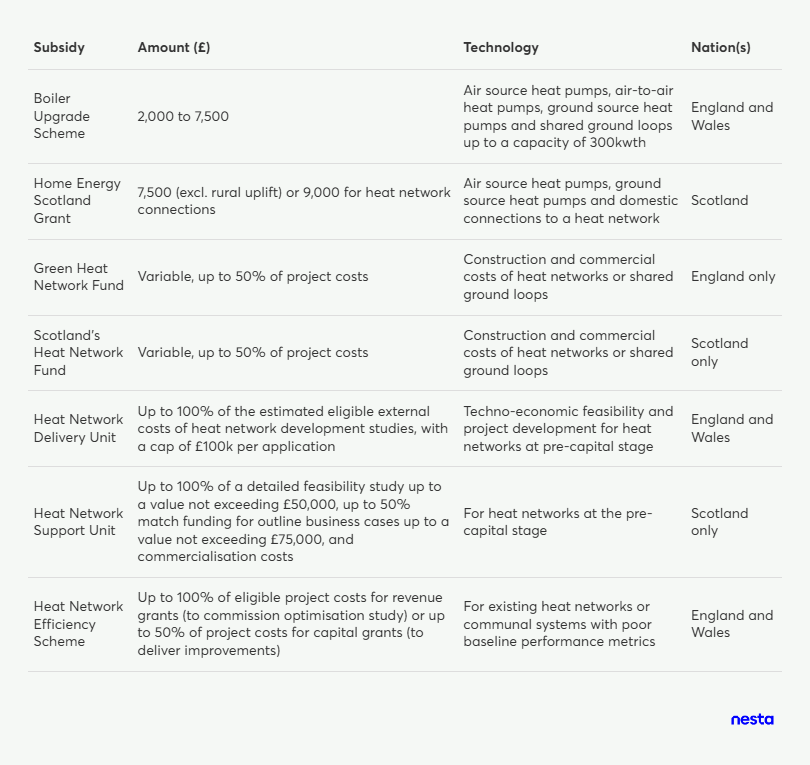

The current subsidy landscape

The UK and devolved governments have used subsidies to increase demand for low-carbon technology, with subsidies categorised by tenure and technology type.

The Green Heat Network Fund (GHNF) and the Scottish Heat Network Fund (SHNF) are competitive funds, and projects must submit a business plan alongside evidence of engagement with offtakers. Neither fund covers upgrades to individual homes (also known as tertiary distribution), but both cover costs down to customers' heat interface units. As of 2025, the Scottish government also provides a grant to consumers to cover domestic connections to heat networks.

By subsidising heat networks up to 50%, the GHNF and SHNF have the potential to de-risk heat networks and increase investor confidence. However, in practice, some stakeholders mentioned structures such as decentralised ambient ground loops (where heat pumps are located in users' homes) had been deemed to be at risk of double funding via GHNF and the Boiler Upgrade Scheme (BUS), and could be less competitive in GHNF applications. It's also worth noting that, at the time of writing, Wales can only access funding through the Heat Network Delivery Unit (which covers feasibility studies) but is not part of the GHNF. For existing heat networks, the Heat Network Efficiency Scheme offers support for upgrades to underperforming heat networks.

The clean heat subsidy landscape takes a siloed approach to technologies and tenures which has impacted local authorities looking to decarbonise their areas. Feedback from stakeholder suggested projects had therefore tended to focus on easy-to-reach tenure types, such as social housing, but left out certain tenure and technology types – in particular, we heard from multiple stakeholders that infilling for residential areas on the edge of heat network zones remained a challenge.

Market models and ownership structures

Three broadly distinct market archetypes for clean heat neighbourhood schemes in the UK emerged from interviews and research.

Public-led and owned model

In this model, the delivery and ownership for a clean heat scheme lies with a public body, such as a local authority, which scopes, leads and secures funding for a scheme.

The public body can fund the initiative either by using its own reserves, accessing external funds through borrowing from institutions such as the Public Service Works Loan Board or national infrastructure banks, or accessing public grants.

In this model, the public body that leads the project can secure a long-term income from the asset through heating bills and service charges paid by consumers. They create long-term, publicly owned assets that can generate other co-benefits in the local area.

However, such projects also place financial pressure on local authorities, who must secure any debt against their assets. As a result, this model is a better fit for local authorities with large housing stocks. Interviewees also noted that borrowing costs had increased for local authorities, with the Public Works Service Loans Board offering more favourable rates for social housing, but not for clean heat developments.

Case study: Cardiff Heat Network

Cardiff Heat Network uses waste heat from an energy-recovery centre, and was recently connected to a newly converted block of 78 flats.

Capacity 15 megawatts

Technology Fourth-generation heat network

Heat source Energy from Waste (Viridor Energy Recovery Centre)

Ownership model Managed by Cardiff Heat Network Ltd., a subsidiary company owned by Cardiff City Council

Funding Through Heat Network Investment Programme and a loan from the Welsh government

Other examples include Pimlico District Heating Undertaking (owned by Westminster City Council in London), Energetik (wholly owned by Enfield Council in London), and the West Dunbartonshire Energy LLP (wholly owned by West Dunbartonshire Council, and operating the Queen's Quay heat network in Clydebank).

Private-public partnerships

In this model, a public body and a private company come together in a joint venture to deliver clean heat, at a local scale (such as a social housing development) or at strategic scale for a city or local area. This model is broad, and encompasses several ownership models, either giving the public or private partner a majority share. It may also accommodate a 50-50 involvement or a golden share structure, enabling the public body to retain privileged control over the outcome of a clean heat project.

This model can lend itself to different legal arrangements, such as a Special Purpose Vehicle, or a concession model whereby the public body grants exclusive access to a private company to deliver clean heat and/or other decarbonisation projects.

This model allows a local authority to minimise financial risk by bringing in private investment through a partnership. For example, in a concessionary arrangement, a private company will shoulder the main commercial risks associated with the project. This model may also include a set of protections and benefits for the local community, including rights of first refusal against projects and commitment to social value.

It also gives the public body strategic oversight of the scheme's goals, but may offer fewer opportunities for scrutiny than in a public-led project. The procurement process may however be resource intensive and bring complexity to the project. A stakeholder also noted that, while scaleable, this model might also be more accessible to a local authority or region with assets for development, and came with legal and governance costs.

Case study: Bristol City Leap

Bristol City Leap is a partnership between Bristol City Council, Ameresco Ltd. and Vattenfall UK Heat Ltd. to accelerate decarbonisation across the city.

Its activities include clean heat and energy generation.

Technologies Heat network (managed by Vattenfall), heat pumps, wind and solar electricity generation

Ownership model Special Purpose Vehicle that grants Ameresco a 20-year contract to coordinate retrofit projects across the city, including subcontracting Vattenfall to manage all heat network operations

Funding Heat Networks Delivery Unit and private capital

Many of the local authorities that have been developing potential future heat networks through the Department for Energy Security and Net Zero's (DESNZ) Advanced Zoning Programme have chosen to procure strategic partners. These include Liverpool, the City of London Corporation and Stockport Metropolitan Borough Council.

Private sector-led

In this model, a private company independently takes the lead on developing and delivering a clean heat project. No involvement is required from a public body in the delivery stage. However, this does not necessarily mean that this model is entirely privately funded (for example, a group purchase of heat pumps managed by a private company would still require households to apply for the BUS).

This model may operate through a company or consortium of companies. Heat may be the company's sole objective or a co-benefit of another structure, such as waste heat recovery from a datacentre or energy recovery facility.

In a private-led project, the financial risks associated with the development and maintenance of assets fall entirely with the company leading and scaling the project. This last option may lend itself to innovative business models but may limit long-term benefits to the local community, as the local authority has no oversight of the company's plans. They may also lead to companies prioritising easier projects such as new-build developments – over more complex retrofit (infilling) projects that bring greater commercial risks to the developer and may not guarantee a good return on investment.

Case study: Melbourn Energy Superloop

Currently in the planning stage, the Melbourn Energy Superloop project in Melbourn, Cambridgeshire is managed by a consortium of companies including DataGlow. It is a combined heat-and power project that includes the generation of energy to power a data centre owned by DataGlow. Waste heat from the centre will be collected via an ambient ground loop and distributed to households through ground source heat pumps.

Technologies Solar panels, data centre, ambient ground loop and ground source heat pumps.

Ownership model The data centre and ambient ground loops will be owned by DataGlow.

Funding Private capital (from Octopus Energy Generation) and public funding (customers will need to apply for the BUS)

What are the current economic blockers to area-based clean heat schemes?

Summary

- Shared-infrastructure projects require large amounts of upfront capital and offer only long-term returns, so they are struggling to attract significant public or private investment.

- The success of securing investment for an individual shared infrastructure project is determined by the potential for the project to produce returns for investors.

- The best way to guarantee stable returns is to create certainty on the number of customers the infrastructure will be able to secure.

- The difficulty in funding individual projects has led to a sector wide 'pipeline problem' that is further limiting the amount of external or new investment for shared infrastructure.

- Projects with a focus on domestic connections, and particularly domestic retrofit, are among the most challenging to fund.

Regardless of the ownership and delivery model of a project, shared infrastructure for clean heat projects requires significant capital expenditure. Meeting UK government targets for the expansion of shared clean heat infrastructure will therefore require significant amounts of capital investment in the sector in the next 25 years. It is unlikely that this will be possible without introducing new investment actors into the sector who can support large project portfolios and delivery at scale. This could be achieved by investing in individual projects or by investing in companies or organisations that deliver clean heat infrastructure.

A range of investors can fill this role, including private financial institutions such as pension funds and investment banks, or public investment bodies such as the National Wealth Fund. Shared infrastructure for clean heat should be an attractive investable asset for these actors, as they can generate long-term stable returns and should be similar to currently investable assets such as gas and electricity networks.

A recurring theme in stakeholder interviews was the observation that major financial actors are not entering the clean heat sector at the necessary speed to enable scaled infrastructure delivery. The high costs of currently available capital restrict the scaling of existing projects and prevent many new initiatives from launching. Our discussions revealed that difficulties with financial models for individual projects have created a vicious cycle of sector-wide barriers that impede affordable capital from entering the sector at the scale required for delivery against national targets.

Blockers for individual projects

A strong business case is vital when determining an investment decision for a shared clean heat infrastructure project, regardless of the financial model that is being pursued. This strength depends on the project's ability to generate a reliable Internal Rate of Return (IRR). Unlike static profit margins, the IRR represents the annual rate of growth an investment is expected to generate, accounting for the timing of cash flows. For long-term investors such as pension funds, the IRR is one of the most important metrics for an investment because it accounts for how much money is made and how quickly it is returned over a period of 25 to 40 years.

A project will reach an investable IRR when the income from customer heat payments successfully covers both the initial capital expenditure for the infrastructure, the ongoing operational costs of heat generation, and the cost of financing. When an investor is confident these long-term revenues are secure, they view the project as lower risk and can offer cheaper capital through lower interest rates. Affordable capital is essential to getting projects to deliver at a larger scale. Stakeholders have identified customer uptake as the main driver that determines the quality of a project's business case, with other factors such as subsidy levels and the cost of heat that a project can offer being important but secondary factors.

Guaranteeing uptake

Stakeholders generally agreed that the number of connections a shared clean heat infrastructure can secure is the key determining factor as to whether a project can attract enough investment to be successful. Being able to guarantee uptake and demand provides certainty on the timeline and size of the return investors can make from the initial capital cost of building shared heat infrastructure. For greater certainty in the earliest phases of designing a district heating system, developers commonly use a rule of thumb metric called Linear Heat Density (LHD). LHD is used to initially determine if there is likely to be sufficient heat demand to make a project financially viable, before considering other factors such as the cost of accessing a heat source or any specialised pipework. While used most commonly in district heating, LHD can similarly be applied to shared ground loops and other types of shared clean heating infrastructure.

Linear Heat Density (LHD)

Linear Heat Density = Annual Heat Demand (MWh/yr)

-----------------------------

Total Pipe Length (m)

Annual Heat Demand (Megawatt hours per year): The total annual demand for heat from heat network connections Total Pipe Length (metres): The total length of pipe used in the heat network

A high LHD is desirable for developers because it demonstrates that more heat can be sold for every meter of pipe installed. This proof maximises the direct revenue that can be generated by the network, leading to a greater return on the initial investment. Consequently, to achieve an optimal LHD, developers strive to secure a heat demand for their projects that is not only the highest possible, but also the most reliable over the long term.

A common approach for financially de-risking a new district heating scheme is the securing of 'anchor loads'. These are large-scale heat consumers, typically non-residential or substantial multi-unit residential buildings, that commit early to purchasing heat from the network. Common anchor loads are hospitals, university campuses, large public sector buildings, leisure centres or major social housing developments.

Anchor loads offer significant, predictable and sustained annual heat demands. By securing commitments from just a small number of these key customers, a project can guarantee a substantial base level of demand. This guaranteed revenue stream improves the business case for the network, making the project more attractive to potential investors and lenders, and enabling developers to secure the necessary financing for the significant upfront capital expenditure required for network construction. Furthermore, the commitment of a major institutional customer can lend credibility and momentum to the scheme, potentially encouraging smaller or residential customers to connect once the network is operational.

However, a reliance on anchor loads is not without considerable risk. If a major anchor load customer later withdraws their commitment, delays connection or significantly reduces their heat demand due to energy-efficiency upgrades or changes in operational needs, the financial viability of the entire scheme can be jeopardized. For example, in September 2025 a deal to deliver a heat network as part of the Granton redevelopment in Edinburgh was terminated in part because the developer had a 'lack of confidence in customer connections'.

Heat demand is easier to guarantee for new builds and redevelopments, and clean heat infrastructure for these types of housing development was identified as much more investable by stakeholders. New builds and redevelopments often lack an existing connection to the gas network, with developers needing to decide whether they pay for homes to be connected to the existing gas network or they install clean heat infrastructure. An Independent Gas Transporter (IGT) interviewed as part of this project reported that the costs of installing a heat network are comparable to installing new gas pipes. The restriction on installing fossil fuel-based heating in new homes as part of the New Build Heat Standard in Scotland and the coming Future Home Standard in England will further increase the appeal of shared clean heat infrastructure for new builds.

The need to maximise reliable sources indicates why there is often a poor business case for shared infrastructure focused on retrofitting private domestic buildings with an existing gas connection. As individual households have low individual heat demands, a large number must connect to a heat network to ensure a sufficient annual heat demand. The requirement for a large number of households in an area to choose to switch to a shared infrastructure solution presents a major risk for a project's financial viability, and makes investors wary about committing significant upfront capital to projects with a large private domestic component.

Cost of heat

Stakeholders also highlighted the cost of generating heat as a common blocker for projects. A project can make a stronger business case if it can offer a lower cost of heat to potential customers than their existing heating (primarily gas boilers in a domestic setting). If the cost of heat is lower there is greater potential for more customers to choose to connect to the network, and that the network reaches the number of users needed for financial viability. The primary reason it is challenging for developers to achieve cost parity with gas is the 'spark gap', or the cost of electricity relative to gas. The energy centre that generates heat for a heat network will often use significant amounts of electricity, for example to power a heat pump. This is why projects will often aim to find ways to generate heat more cheaply, such as using waste heat or co-locating with a renewable energy generation site. If projects are unable to reduce the cost of generating heat they will be forced to either rely on large anchor loads to offset the risk of poor private domestic uptake, or offer other incentives for consumers to connect to the network, such as the Octopus Superloop, whose consumer deals feature broadband and a fixed-cost tariff.

Subsidy landscape

While public subsidies are crucial for de-risking clean heat projects for private investors, the current public funding landscape remains challenging. The GHNF, the primary existing source for supporting heat networks and shared ground loops, is highly competitive and oversubscribed, which creates uncertainty for individual proposals that are seeking funding. Stakeholders have also highlighted specific issues with the GHNF, particularly for projects that struggle to attract private investment, noting inadequate provision for schemes focused on domestic users and those involving shared ground loops.

The pipeline problem

Stakeholders said the challenges faced by individual projects compound at a national level, creating a ‘pipeline problem’. A ‘pipeline’ refers to a series of projects planned at a national or local level. A clear long-term pipeline was seen by stakeholders in private investment and both the public and delivery sectors as key for creating the certainty and predictability that will unlock more upfront capital for infrastructure projects, and facilitate more ambitious development. New investors and more capital were seen to be essential to scaling delivery in line with the UK government target to have 20% of national building heat demand delivered by shared heat infrastructure by 2050. DESNZ estimates that the heat network sector alone may have an investment potential of between £60 billion to £80 billion by 2050.

At present, it is estimated that only between 500,000 and 900,000 households in the UK are currently connected to a heat network, which accounts for roughly 3% of national heat demand. Planned connections for new heat network projects currently under or awaiting construction in Q4 2025 (as documented in the DESNZ's Heat Network Pipeline Database) total only 76,712 where electricity is cited as the main planned heat source, with the average number of connections for an individual project being 201. To reach national targets from this starting point the UK will require shared heat infrastructure to be delivered in a coordinated way across geographies and communities, and not always in the most ideal of economic conditions. A key part of reaching this target will be delivering shared heat infrastructure in urban centres, with the Warm Homes Plan estimating that over 50% of heat demand in Manchester and London could be best met by district heating. Urban heat networks will be large infrastructure projects that individually could require investment into the hundreds of millions.2

Currently, however, stakeholders identified that clean heat infrastructure projects most commonly happen as 'one-off' initiatives. These projects are typically smaller, both in terms of heat output but also in terms of capital expenditure requirements, such as rural projects like the Swaffham Prior heat network, whose development represented a total cost of £14 million and connected only 100 households. Current projects also likely have unique success factors that make their business cases especially strong, such as being focused on new builds or co-located with a newly developed source of waste heat, like a data centre. This series of disconnected and smaller-scale projects typically rely on smaller investors or are self-financed by those delivering the project. They often do not attract the large institutional investors such as pension funds, who are generally interested in much larger assets, with stakeholders indicating they were looking for portfolios of projects in the £100 million plus range. Large public sector investors are similarly looking for larger investments, for example the National Wealth Fund has a minimum investment or ‘ticket size’ of £25 million.

In addition to keeping large investors away, these small projects prevent the delivery supply chain from scaling up and maturing. Consequently, a self-reinforcing negative cycle is created, further complicating the delivery of individual projects and severely impeding the possibility of scaled-up deployment.

Some stakeholders believe that developing a national portfolio of smaller projects delivered in the most favourable conditions will organically develop ambitions in local governments and institutional finance to deliver larger more complex projects, with projects in new builds, for example, acting as case studies or proof of concept. However, as reflected in the views of the majority of stakeholders, there is a much deeper, longstanding coordination failure between local government planning and external institutional finance actors that would inhibit the development of a project pipeline, especially one that could deliver in time to meet national targets.

Coordination between local government and institutional finance

Regardless of whether a shared heat infrastructure project is delivered publicly or privately, delivery will involve local government. Local governing bodies will need to approve developments that involve digging up public roads to place pipework while also acting as important sources of anchor load through leveraging public buildings and social housing. This role has become formalised for local government as UK heat infrastructure regulation has designated Heat Network Zones and Local Heat and Energy Efficiency Strategies (LHEES).

Stakeholders noted that despite local government's crucial role, combined and local authorities currently engage in limited delivery-focused planning for clean heat infrastructure. This type of planning, which is often lacking, includes identifying potential waste heat sources and large anchor loads, and designating areas for shared infrastructure development. Local government faces significant barriers, including a lack of necessary tools and resources. Specifically, they lack the capacity and expertise for local heat planning, as well as the legal and regulatory powers needed to incentivize development, such as mandating connections from potential anchor loads.

There was broad agreement among stakeholders that institutional finance actors, both private and public, are interested in the potential of investments in clean heat infrastructure. Stakeholders however identified that without clear local plans and a national trajectory for how shared heat infrastructure will develop, and a portfolio of projects requiring a large initial capital investment, institutional financial actors will remain disinterested in investment. The lack of interest from institutional financial actors then creates a vicious cycle, as local governments are offered few incentives or little external pressure to develop the capacity to support pipeline development. Without a national policy push, it is unlikely that the necessary local government planning and investment interest will coordinate to deliver shared heat infrastructure at scale and at pace.

Lessons from different approaches to infrastructure funding

Summary

- The financial model of clean heat infrastructure shares similarities with lots of existing or emerging infrastructure in the UK, particularly the gas network, broadband and public charging for electric vehicles (EV).

- In supporting clean heat infrastructure to overcome economic barriers, there are key lessons to learn from regulatory regimes and state interventions deployed in the past.

- The long history of the gas network means it is a poor direct comparison to building new heat infrastructure, however it does offer lessons for regulating infrastructure in the future. There may also be a key role for Independent Gas Transporters in transitioning into delivering heat networks.

- As identified in support programmes for public EV charging, infrastructure coordination between different funds and levels of government is important in developing a long-term project pipeline, as is supporting both the supply and demand side of emerging sectors.

- Used to fund high-speed broadband, community voucher schemes could also be used to expand heat networks with limited plans for domestic connection. The Universal Service Obligation could also inspire similar regulation to guarantee consumers access to affordable clean heat.

Although clean heat infrastructure such as heat networks or shared ground loops is an emerging technology in the UK, its economic characteristics closely resemble those of other established infrastructure types. Analysing other sectors presented an opportunity to identify how similar economic barriers to scaling have been overcome. Research as part of this project focused on other types of infrastructure that share key characteristics with shared infrastructure for clean heat. The common characteristics identified were:

- Have elements of a natural monopoly

- Require large amounts of upfront capital

- Offer long-term returns

While no single other type of infrastructure is a direct analogue for clean heat infrastructure, there are key lessons to be learnt from other sectors. The development of the gas network, public electric vehicle (EV) charging stations and publicly subsidised broadband provided the most relevant examples of overcoming economic blockers.

These types of infrastructure have managed to build strong business cases for individual local projects that have led to a strong national pipeline of development projects.

Gas network

In terms of function, delivering heat to households, the clearest comparator infrastructure for clean heat shared infrastructure is the UK gas network. The gas network is one of Britain's largest infrastructure assets, both in terms of value and physical size. It encompasses over 280,000 kilometres of transmission piping, as well as a range of supporting infrastructure spread nationwide. This network has been built over two centuries, and in that time has transitioned through various models of ownership and a range of transportation technologies, requiring huge amounts of capital investment while also generating significant returns for investors, both public and private. The gas network requires constant maintenance and has been expanded over time, the regulatory and financial structures that facilitate these ongoing projects have some instructive lessons for financing clean heat infrastructure, including the potential role of Independent Gas Transporters (IGTs). However the gas network has benefited from centuries of state investment and its monopoly position means it may primarily serve as a model for how shared heat infrastructure may be regulated in future if it scales nationally.

The gas network is made up of two main components, the National Transmission System (NTS), the national series of pipelines that transport gas at high pressures from natural gas terminals to large industrial users, and the local distribution network. The latter is made up of eight regional Gas Distribution Networks (GDNs): a series of smaller pipes and supporting infrastructure that receive natural gas from the NTS and transport it at lower pressures to smaller business and domestic consumers. While the GDNs make up the majority of the local gas distribution network in the UK, in a small number of areas Independent Gas Transporters (IGTs) own separate local gas infrastructure. As of June 2025, there were 15 IGTs in the UK, which are not geographically bound and own small networks nationwide.

The UK gas network was privatised in 1986. Prior to this it was owned and managed by the wholly state-owned British Gas Corporation, with the maintenance or expansion of any gas infrastructure financed by the UK government. In the four decades since then, the ownership of the NTS and local transmission networks has moved from being entirely owned and operated by a privatised British Gas to its current position, where the ownership of the NTS and local gas distribution networks is spread across many different private companies.

The NTS is now owned by National Gas, a private company owned by a consortium of international investment firms and pension funds. After being sold by the National Grid in 2005, the eight GDNs are now owned by four different private companies, which themselves are owned by a range of international investors, including utility companies in other countries, pension funds and investment firms. The UK's 15 IGTs began as private companies. Typically, rather than buying pre-existing gas infrastructure assets, the IGTs have built their own privately financed gas infrastructure, having been granted licences to do this beginning in the 1990s. IGTs often build connections for areas not yet connected to the gas grid, for example for new housing developments.

As privatisation only occurred in 1986, the original capital expenditure for lots of gas infrastructure in the UK was financed by the state. The private companies that, from 1986 onwards, bought the then existing network assets generate a financial return by charging gas suppliers (the energy suppliers consumers pay bills to) to transport gas from supply to end use.

As the gas network is a natural monopoly, the sector is tightly regulated and companies have a legal obligation to maintain and expand the gas network over time.

These maintenance and expansion projects are often very similar to projects for building clean heat infrastructure; they require digging up trenches, laying pipework and significant upfront capital investments with a long payback period. As GDNS and IGTs deliver gas directly to domestic consumers they are more comparable to shared heat infrastructure than the NTS.

GDNs typically self-fund investment in the network, whether this be by securing additional private investment, corporate debt, using capital reserves or accessing certain central government funding schemes. They are able to recoup these investments through increasing their charges on gas suppliers using their gas network, who then in turn increase the energy bills of their customers. The investments GDNS make are used by Ofgem to calculate the GDN's Regulated Asset Base (RAB). The RAB is used in addition to the RIIO (see p.7) framework to determine how much revenue the GDN is able to generate through charges on consumer bills, and therefore the payback period of the investment. The size of GDN regions mean that investment costs can be spread across millions of customers, making the amounts eventually added to bills relatively small. This small payment from individual households as well as the RAB and RIIO frameworks allow GDNs to offer external investors a high degree of certainty as to the return period for investments and can allow them to access relatively cheap debt.

IGTs are regulated differently from GDNs and do not operate under the same RIIO or RAB frameworks. IGTs will also self-fund any capital investment projects, through either acquiring debt or, as they are often working on new-build projects, through a partnership with a housing developer. They will then apply costs to gas suppliers that are passed on to consumers. The Relative Price Control (RPC) regime ensures that the charges IGTs levy are capped at a level relative to the GDN charges in that local area. Similarly to the RAB and RIIO, the RPC creates certainty for IGTs and their investors on the rate at which they will recoup costs from investments.

Independent Gas Transporters (IGTs) and heat networks

Some IGTs (e.g. Energy Assets and Leep) have begun to position themselves not just as gas transports but as 'multi-utility' distributors. This includes expanding into financing, delivering and owning clean heat infrastructure, particularly heat networks. As the use of natural gas for home heating declines, IGTs have a growing need to invest in alternative assets and diversify their business model. While some IGTs are prioritising work to repurpose existing pipe work for bio-gas or hydrogen, others are choosing to use their existing technical experience to branch into clean heat infrastructure. Conversations with stakeholders identified why IGTs are well placed to take on clean heat projects:

- They already have business models built around owning and maintaining assets with similar expenditure and return profiles, i.e gas networks.

- They have extensive experience and capacity to deliver much of the construction and civil engineering work needed for heat networks, i.e digging trenches, and installing and designing pipework.

IGT stakeholders involved in delivering heat network projects identified that the sector is currently focused on delivery projects for new builds and redevelopments. This focus is driven by two main factors: the improved business case that results from guaranteed customer uptake in areas lacking an existing gas network, and the opportunity to leverage established relationships with housing developers. Stakeholders were optimistic that successful projects in this new-build and redevelopment space would serve as valuable case studies, potentially paving the way for future, inherently 'riskier' retrofit projects.

The regulated financing mechanisms for both GDNs and IGTs are effective at facilitating long-term planning and investment for the maintenance and upgrading of network assets. Crucially, however, these models are underpinned by large user bases and highly certain demand. Models like the RAB, RIIO and RPC require user demand to be highly predictable, and could be applicable to share heat infrastructure when it is widespread nationally.

Public electric vehicle charging

Infrastructure for publicly accessible electric vehicle (EV) charging shares many characteristics with shared heat infrastructure. A novel infrastructure asset in the UK, it has been a government priority to expand its reach to facilitate wider EV adoption. Public EV chargers are chargers in public locations, such as a residential street, that can be used by anyone, typically in exchange for a charging fee. A public EV charger can provide long-term returns for its operator, after an initial capital investment in installation (though this is much lower than for shared heat infrastructure) and ongoing payment to supply the charger with electricity. The returns of an EV charger are inherently unpredictable and reliant on the number of drivers who choose to use them, though they can also be installed in small batches and expanded based on demand. Like heat networks, EV charging is also an emerging technology in the UK and one that has a limited pool of existing users to guarantee uptake. The UK has achieved a rapid expansion in prevalence from less than 2,500 public EV chargers in the UK in 2015 to over 76,000 in 2025. Public EV charging was seen by the UK government as a priority for increasing the uptake of EVs. There was a limited existing domestic supply chain or business base for delivering EV chargers at scale. UK government policy has been key in simultaneously stimulating demand and supporting business development to achieve this rapid expansion.

Public EV chargers can be owned and operated in a range of ways. Some public EV chargers are installed on private land, such as in a supermarket car park. In these cases a private operator is responsible for the upfront cost and any associated maintenance, but also recoups most of the payments from users. To ensure widespread access to chargers, especially on-street charging in residential areas, it is often necessary for chargers to be installed on publicly owned land, such as on residential streets. Typically, this land is owned and managed by local authorities. Local authorities can choose to either own and operate the chargers themselves or allow external operators to install and manage the chargers via a lease or concession agreement. EV charging infrastructure on local authority owned land offers the strongest parallel to clean heat infrastructure, as this is typical of the types of residential areas heat infrastructure will need to be built in.

To stimulate demand for public EV charging infrastructure, UK government strategy leveraged funding to local authorities though the Low Emission Vehicle Infrastructure Scheme, and used the Charging Infrastructure Investment Fund to support businesses in expanding to meet demand. EV charging policy highlights how government-support programmes can be used to support emerging sectors and industries in scaling quickly.

Charging Infrastructure Investment Fund

A £420 million joint public-private investment fund launched in 2017 to 'catalyse the rollout of electric vehicle charging infrastructure', with the specific criteria that 'each Investment shall be made with a view to contributing towards the development of accessible, reliable, self-sustaining and secure electric vehicle infrastructure for cars and vans in the United Kingdom.' The fund combines £200m from the UK government and private capital (managed by Zouk Capital) to build a reliable, open-access, rapid EV charging network. The fund has a ten-year life span, ending March 2030. The investment period for new investments ran until March 2024. The fund focused on scaling up rapid EV charging networks, with early investments including InstaVolt, and later, the support of firms such as Zest for on-street and destination charging.

Low Emission Vehicle Infrastructure Scheme

The scheme provides a £380.8 million fund to assist UK local authorities in deploying public EV charging infrastructure. This total is split into £343 million of capital funding for the direct cost of chargepoint delivery, and £37.8 million of capability funding. The latter sum is specifically designated to allow local authorities to hire and train new staff to plan and execute the chargepoint infrastructure rollout.

Tier 1 local authorities are given funding allocations depending on the current number of local EV chargers and vehicles without off-street parking, as well as deprivation and rurality metrics. Local authorities can then apply for funding for specific projects and developments.

This coordinated support for all levels for sector development could be applied to shared heat infrastructure, with direct investment in delivery and support for local authorities to create demand.

Publicly subsidised broadband

The UK broadband network is the physical telephone cables, ducts, cabinets and exchanges that facilitate broadband connections across the UK. The country's broadband network is owned entirely by private companies. Developed over time, this network has its physical origins in the UK telecom network, which was constructed by British Telecom (BT) under public monopoly until BT was privatised in 1984. Since then, most of the development of the UK broadband network has been undertaken by BT using private capital. The infrastructure for high-speed broadband, such as fibre-optic cables, was therefore delivered entirely during privatisation. This means that the tools and subsidies the UK government has used to encourage the universal development of infrastructure for high-speed broadband (even when the business case is poor) offers a key model for developing high-cost infrastructure in scenarios where there is a probability of market failure.

BT still owns the majority of the UK's broadband network, however competition was introduced into the market through the entrance of other companies, initially Mercury Communications, though today the main competitor is Virgin/O2. In 2005, BT was required to spin-out its network-maintenance functions into a subsidiary: Openreach. This was supposed to encourage competition in the sector. Similar to gas suppliers and GDNs/IGTs, Internet Service Providers (ISPs) pay the network owner to offer broadband as a service to customers and then manage customer relations and billing.

Universal Service Obligation

The Universal Service Obligation offers legal protection for consumers in relation to their home being able to connect to ‘high speed’ internet. Introduced in 2023 for broadband, and expanding on existing legislation for telephone services, any home or business in the UK is able to request a new or upgraded broadband connection if they:

- have no access to existing ‘decent’ broadband (a download speed of at least 10 Mbit/sec and an upload speed of at least 1 Mbit/sec); and

- will not be covered by a public broadband scheme offered by the UK or devolved governments in the next 12 months; or

- have access to 'decent' broadband but it costs more than £57.60.

The cost of the new or upgraded connection for the home or business will be covered up to £3,400, with the option for the customer to pay the excess.

In 2019 the UK government set a target of delivering gigabit-capable internet to all households by 2030. The majority of this infrastructure development can be delivered entirely privately, with the capital expenditure private providers need for the cost of network upgrades able to be recouped from the revenue they will generate from customer bills. However, it was estimated that 20% of UK households fall into the 'hard to reach' category, where there is a poor economic case for upgrading connections. It will require significant capital expenditure to enable these properties, often in rural areas, to be upgraded, with work, such as digging miles of trenches, sometimes having the potential to connect only a small number of households. Connecting these ‘hard to reach’ households is not commercially viable for companies such as Openreach or Virgin/02.

In 2021, to address market failure in regions where private investment alone cannot reach, the UK government launched Project Gigabit, a £5 billion strategic intervention designed to deliver connectivity for the 'final 20%'. This included the Gigabit Infrastructure Subsidy (GIS), subsidy contracts for private companies to deliver network upgrades for specific geographic areas. The subsidy reduces upfront capital risk by providing ‘gap funding’, capital grants that cover the financial deficit between the total cost of construction and what a private provider can commercially justify based on projected long-term subscription revenues. This ensures that while the infrastructure remains privately owned and operated, the initial capital expenditure is publicly de-risked, preventing a digital divide and providing a blueprint for how other high-capex utilities, such as heat networks, can overcome the hurdle of massive upfront infrastructure costs.

The Project Gigabit programme also delivered the Gigabit Broadband Voucher Scheme. This gave households and businesses in communities in hard-to-reach areas outside of the large geographic regions supported by the Gigabit Infrastructure Subsidy access to small grants, which could be pooled and used to develop plans for network connections with private network providers. A voucher system offers another approach that could be used to support consumers to generate demand for infrastructure that has a high initial capital cost and long-term payback.

Policy opportunities for area-based approaches to clean heat

Summary

- New policy developments in clean heat represent opportunities to increase investor and consumer confidence, which could stimulate private capital.

- The Warm Homes Plan, Heat Network Zoning policy and Local Power Plan signals the UK government's support for a more coordinated clean heat transition but also an increased turn towards financial transactions and a push to increase private investment.

- The creation of new functions, such as zone coordinators, but also bringing in Distribution Network Operators (DNOs) as partners in clean heat delivery, could support local governments with lower capacity in creating and delivering clean heat plans.

- These new functions will need to be supported with funding to function effectively.

Sector-wide barriers have resulted in a slow uptake of clean heat infrastructure at scale. In this section, we appraise the potential of recent policy developments to help de-risk area-based clean heat finance and help the market progress at the scale needed.

The new fiscal framework and its impact on clean heat

At UK level, a raft of policy documents published at the beginning of 2026 contains a range of positive developments for area-based clean heat. The UK government's new direction is characterised by a stronger regulatory approach to shared heat infrastructure, strengthened consumer protections, and the enshrining of a stronger role for local authorities in taking the lead on clean heat.

In a constrained budgetary landscape, this turn to clean heat operates against the backdrop of the UK government's new fiscal framework, often referred to as the 'fiscal rules'. These rules require that day-to-day spending should be covered by revenue (the Stability Rule). Additionally, the Investment Rule focuses on decreasing the size of public sector net financial liabilities, which includes public sector debt and pensions, minus government assets, which include student loans and government equity stakes in private companies. This is relevant to clean heat policy developments. As one stakeholder put it, this approach is reflected in the Treasury pushing government departments away from grant funding and towards financial transactions (FTs): loans or investments expected to produce a financial return, with government funding acting as 'a multiplier for other forms of finance' rather than the sole funder for local projects.

A policy framework for area-based approaches to clean heat: The Warm Homes Plan

The recently published Warm Homes Plan makes a number of provisions to support area-based clean heat and coordinate decarbonisation at scale.

What is changing?

- The UK government will set up a new Warm Homes Agency, which has a mission to advance the delivery of strategic and place-based approaches to clean heat through stimulating demand and investment.

- The UK government will consult on bringing in DNOs as partners in the area-based delivery of clean heat projects.

- The Warm Homes Plan also brings the role of local government into focus as delivery partners for clean heat projects, but does not make explicit provisions about what this role might look like.

- The Plan also confirms the end of the Energy Company Obligation (ECO) and includes £5 billion to devise a new funding offer to low-income households and housing associations.

- It also includes a Warm Homes Fund comprising £5 billion in financial transactions, of which £1.7 billion for low- and zero-interest consumer loans, £0.6 billion of low-income funding and £2.7 billion for innovative finance for investments in and loans to the home-upgrade sector.

- It enforces new Minimum Energy Efficiency Standards (MEES), by mandating an Energy Performance Certificate (EPC) of C for the private and social rented sectors by 2030.

The Warm Homes Fund signals a government shift to area-based decarbonisation, giving local authorities a strategic role in clean heat delivery. It includes a statement of intent to strengthen project pipeline and supply chain development, driving demand through funding and regulations (such as MEES), and placing conditions on the recipients of public grants to procure schemes through former ECO supplier companies.

The Warm Homes Plan also foregrounds a role for the National Wealth Fund in supporting clean heat at scale, but this role has yet to be defined. The National Wealth Fund's recently published strategy suggests that it will primarily support the strategic development of heat networks through its Regional Project Accelerator. It is expected this will be achieved by using debt financing and guarantees but that 'opportunities (...) to provide financing directly to heat network projects are expected to be more limited in the short term'.

Questions and opportunities

- Given low consumer appetite to finance heat pumps through loans, to what extent will the offer of consumer loans help support uptake of low carbon heating technologies?

- How will DNOs work with local authorities, and how will these authorities be resourced?

- Could the proposed Warm Homes Fund support infilling for areas on the edge of feasibility (e.g. just outside of a heat network zone)?

- We heard from some stakeholders that the high ticket threshold of the National Wealth Fund (£25 million) could be a barrier for smaller projects: what opportunities can the Warm Homes Plan create to bridge the gap between smaller projects and finance? Can the Warm Homes Plan support project integration and securitisation in order to help smaller projects reach investable thresholds?

Securing demand: Heat Network Zoning and a changing regulatory environment

As of January 2026, Ofgem has become the designated regulator for heat networks, and heat network operators must seek or maintain their authorisation with Ofgem. This change in regulatory regime also comes with changes to consumer protection guidance, which will apply across the UK. The new legislation includes a fair pricing framework, billing transparency, protection for vulnerable consumers and security of supply. As of March 2025, heat networks have also been conferred rights – similar to those of other utilities – to dig up a road and maintain equipment, lowering construction costs. The Heat Network Technical Assurance Scheme brings in a new standardised framework for technical performance. The UK government has announced its intention to consult on the scheme in 2026. The Warm Homes Plan confirms ongoing funding of £195 million per year for the Green Heat Network Fund up to the end of the current Parliament.

In January 2026, the UK government also released an update to its consultation on heat network zoning, which makes provisions for expanding heat networks in England.

Heat network zoning (England only)

- The policy establishes a Zoning Authority that will support the zoning process nationally, including initially identifying heat network zones. Zone-coordination bodies will be appointed locally, and will oversee the development of heat networks, including administering a competitive process to identify suitable developers for each zone.

- Zone coordination bodies will be co-designed with local authorities to arrive at the most locally-suitable governance structure, and will need to go through a capability test to show they are suitably equipped to take the local oversight of the zoning policy forward.

- The policy gives developers the power to request mandates to connect for certain types of buildings within a heat network zone.

- The policy also includes the ability to mandate the connection of heat sources, such as 'water treatment centres, data centres and waste incinerators'.

- As of March 2025, heat networks have been conferred rights – similar to those of other utilities – to dig up a road and maintain equipment, lowering construction costs.

These measures are intended to lower the cost of capital, by providing further assurance to developers of demand (particularly through the requirement for some buildings to connect) and increasing consumer certainty. Questions remain in the heat network zoning legislation, which currently requires building owners to connect in a heat network zone but does not mandate heat consumption.

Key questions and opportunities

- Can the government use heat network zoning as a model to expand mandates to connect to other technologies, creating zones where shared ground loops or network heat pumps could be declared the most suitable technologies?

- Will heat networks access similar finance regimes to other regulated assets?

- Will the combination of bodies created by the policy be successful in creating local and national pipelines of heat network projects that move forward into development?

The Local Power Plan